Economic Updates for April 2023

Summary

Running on fumes - how long can we go before we hit recession?

It has been quite a month! FED very successfully dodged the banking crisis and got away with raising rates one more time. The market thinks they are likely to raise once again in May.

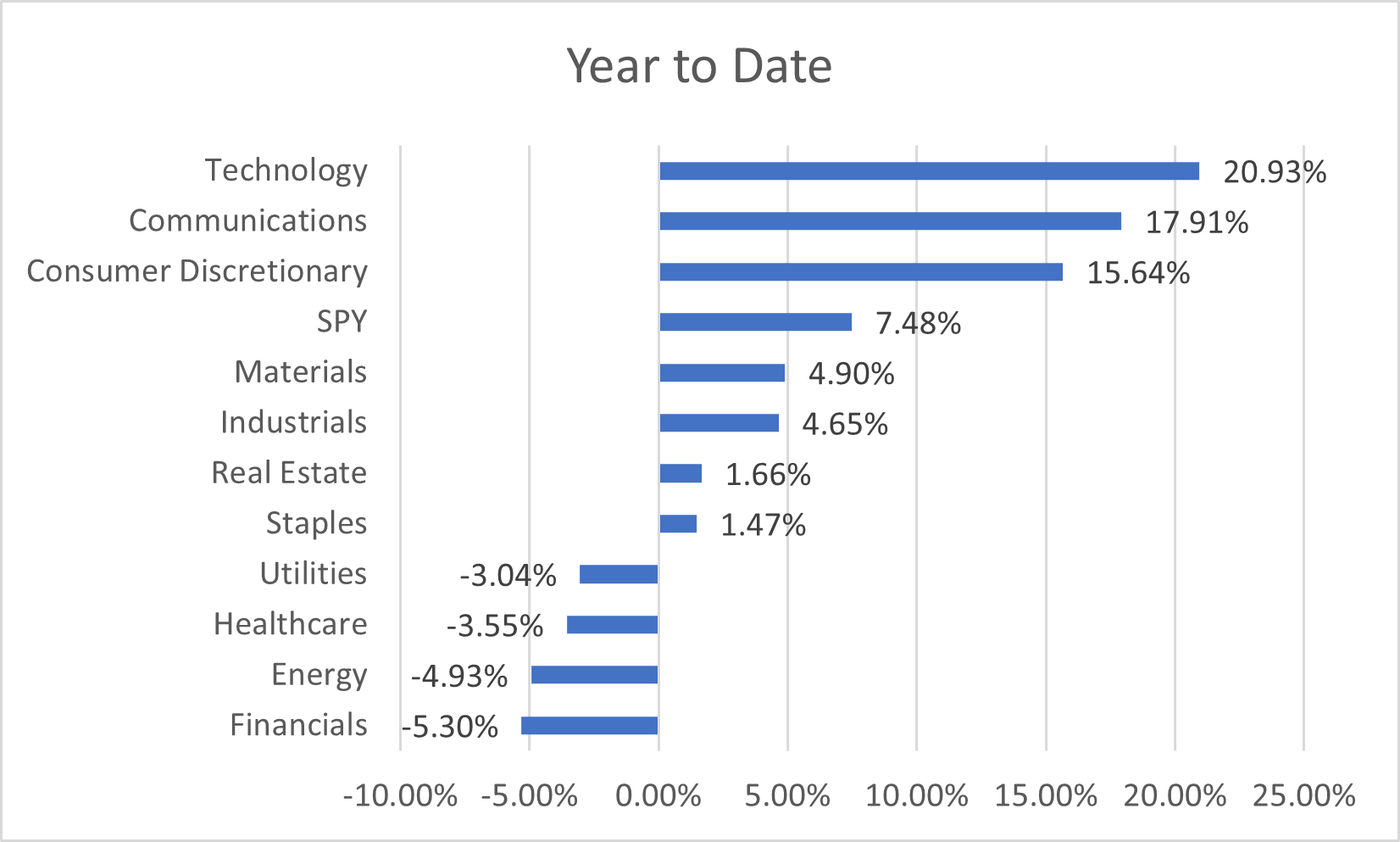

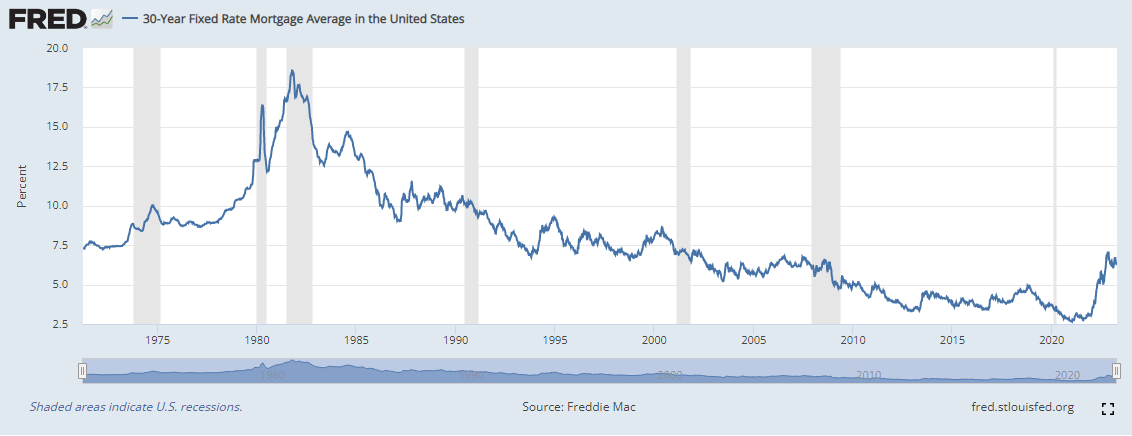

The short end rates have breached above 5% since our last update and is still rising. The earnings season for Q1 2023 is in progress and while earnings expectations have been tempered, most companies so far seem to be able to meet or beat those reduced expectations.

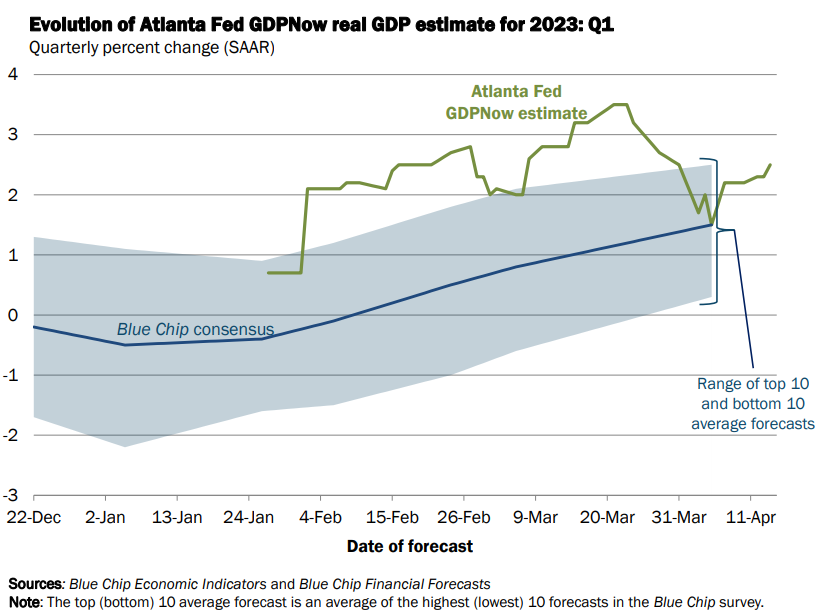

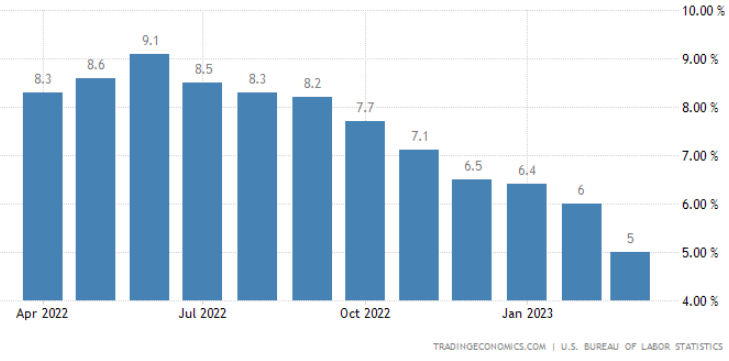

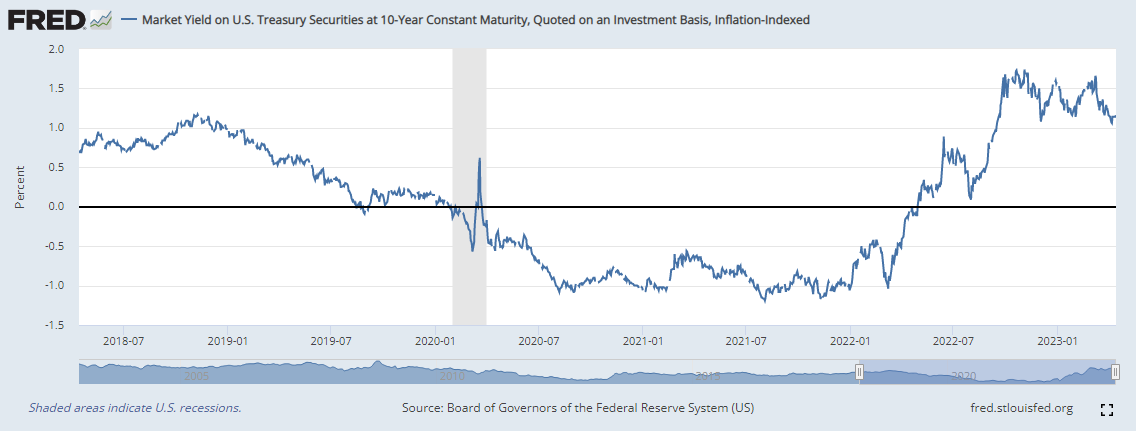

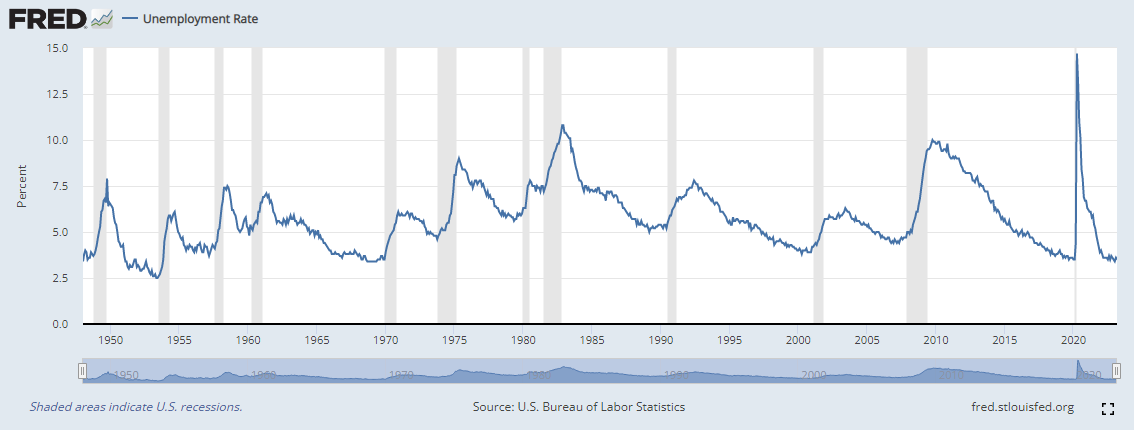

However, none of these indicate continued growth in the coming months / years. In spite of Atlanta FED GDP nowcast projecting 2+% growth for Q1 2023, the market participants are getting more certain of a hard landing where they see a recession ahead - in Q3 2023 or latest by Q2 2024. Their conviction is based on the fall in commercial and industrial loans since the SVB banking crisis. The elevated interest rate takes time to evidence its effects. It is just a matter of time when credit becomes tight enough to slowdown growth and push unemployment rates higher. FED, in fact, is projecting that unemployment will rise by about a percentage point by the end of the year. So, we are running on fumes, and it is just a matter of time before the economy enters a recession.

What if we are wrong and FED is successful in managing a soft or no landing - no recession and the economy continues to make progress? If so, we expect to see the GDP factors to improve and price to earnings ratio of equities to rise. While there is some evidence for both, we are still skeptical.

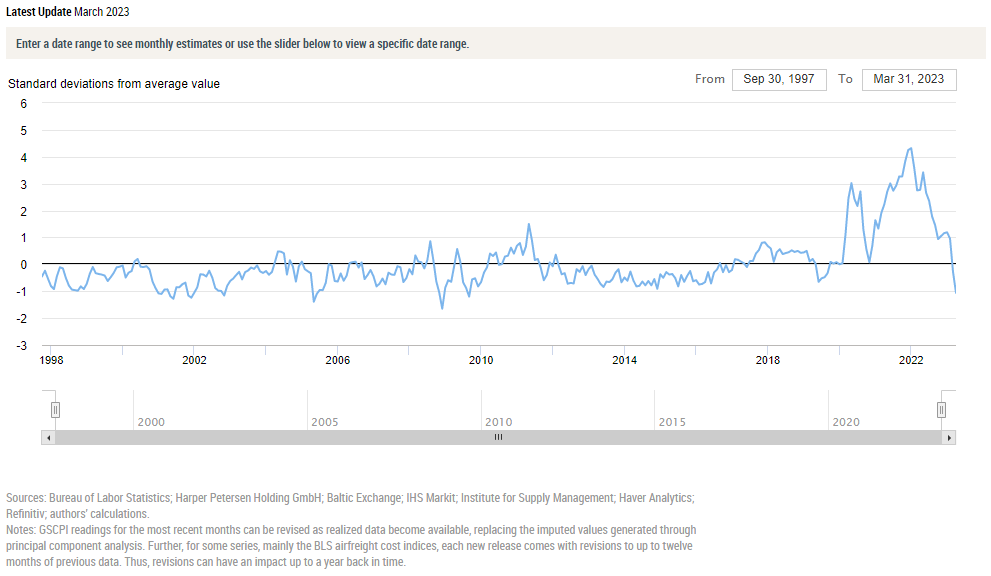

Broad Indicators

Money Market Funds Growth

Atlanta GDP NowCast

US Dollar Index

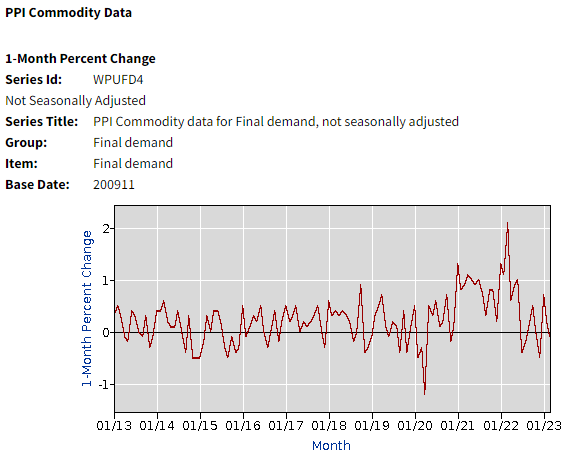

Commodities

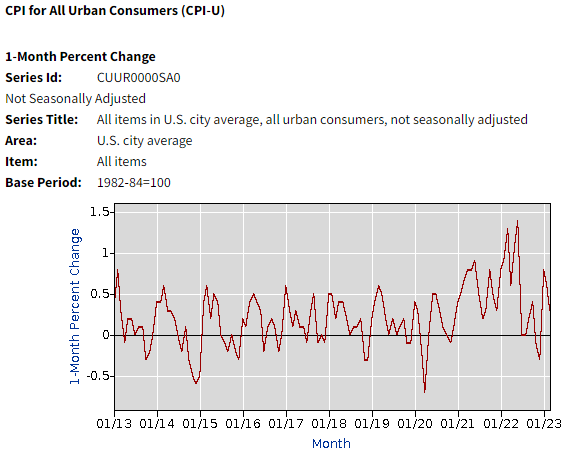

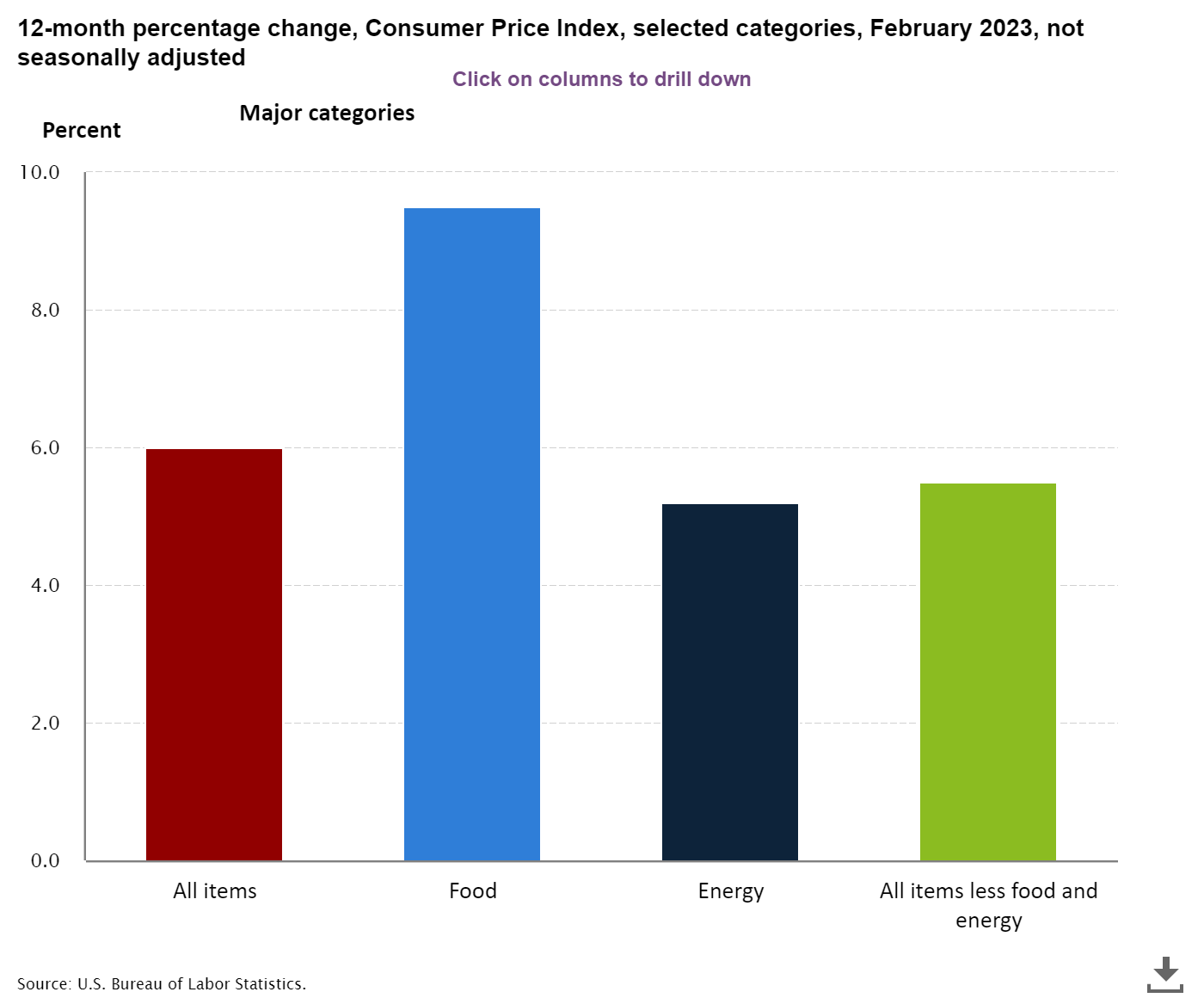

CPI Components Last Month

CPI Components Last Month

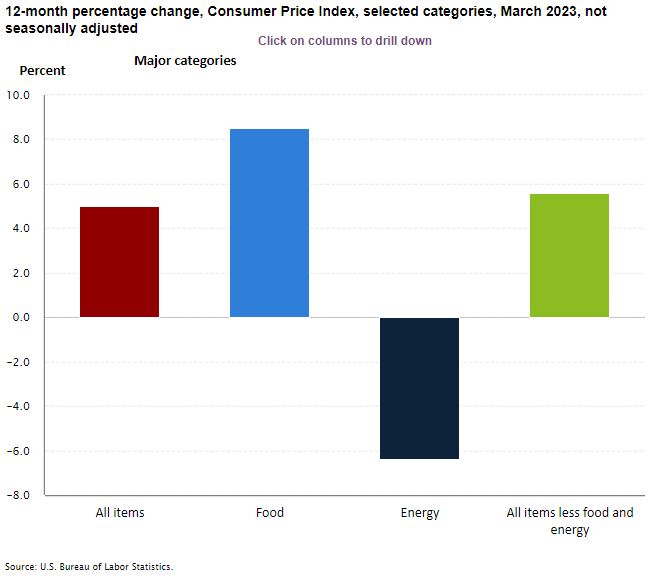

CPI Components This Month

CPI Components This Month

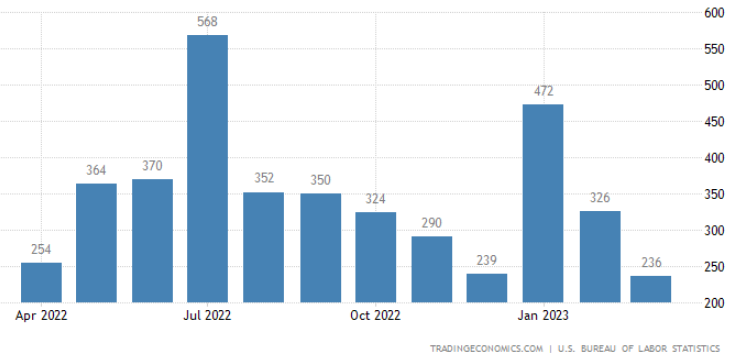

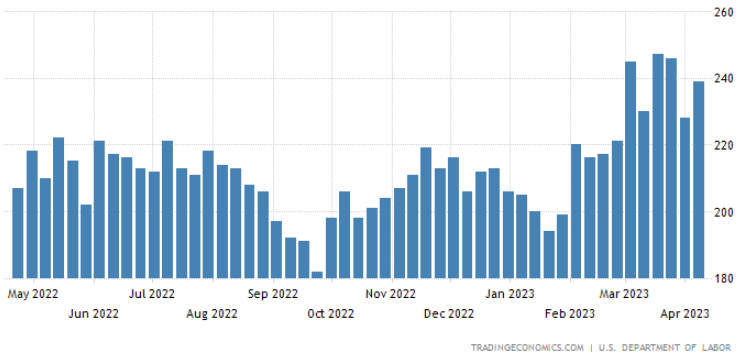

This chart will be the first indicator of a telltale sign that unemployment is increasing. As you see the continuing

jobless claims number rise, it implies the people who lost their jobs are not going back to labor force fast enough

and the unemployment rate is starting to creep higher.

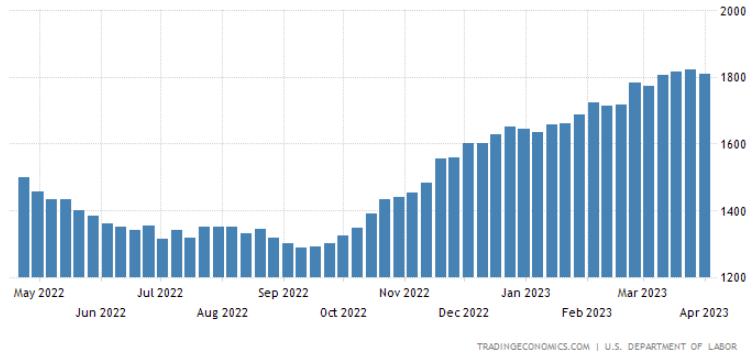

This chart will be the first indicator of a telltale sign that unemployment is increasing. As you see the continuing

jobless claims number rise, it implies the people who lost their jobs are not going back to labor force fast enough

and the unemployment rate is starting to creep higher.

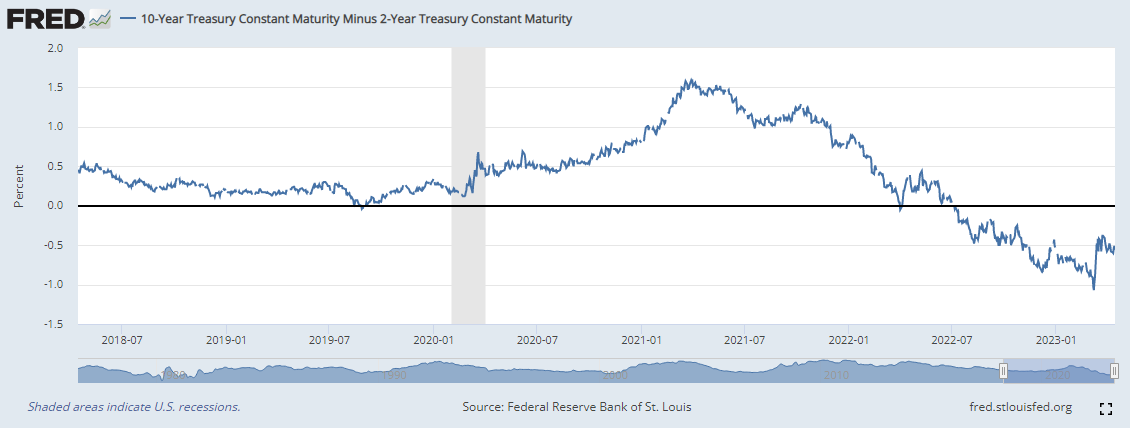

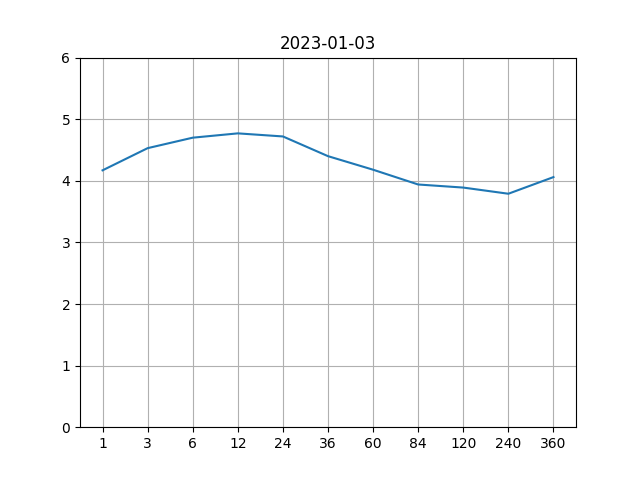

Yield curve - Then

Yield curve - Then

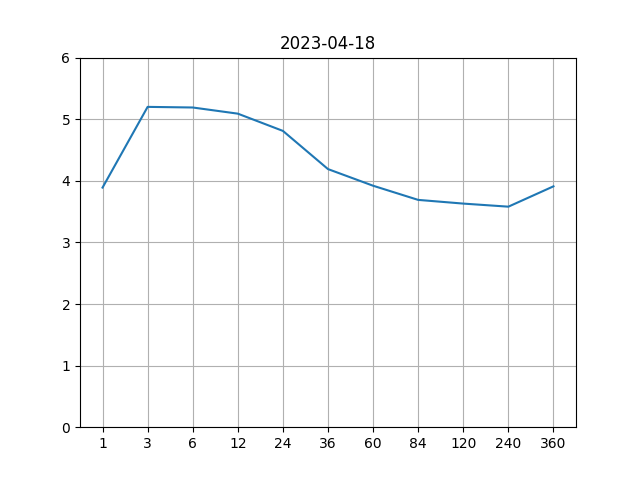

Yield curve - Now

Yield curve - Now