Economic Updates for March 2024

Summary

Economy Stays Strong, Market at New Highs

The economy seems to be firing on all cylinders. The manufacturing index is expanding, job numbers are looking better, energy prices have increased. This has also led to a higher level of inflation. For the past two month, inflation rate has not been gliding down as originally expected.

The state of the economy and the steady rate of inflation may likely cause the FED to sit tight on the current level of interest rates. They may not lower the rates as the market expected earlier this year.

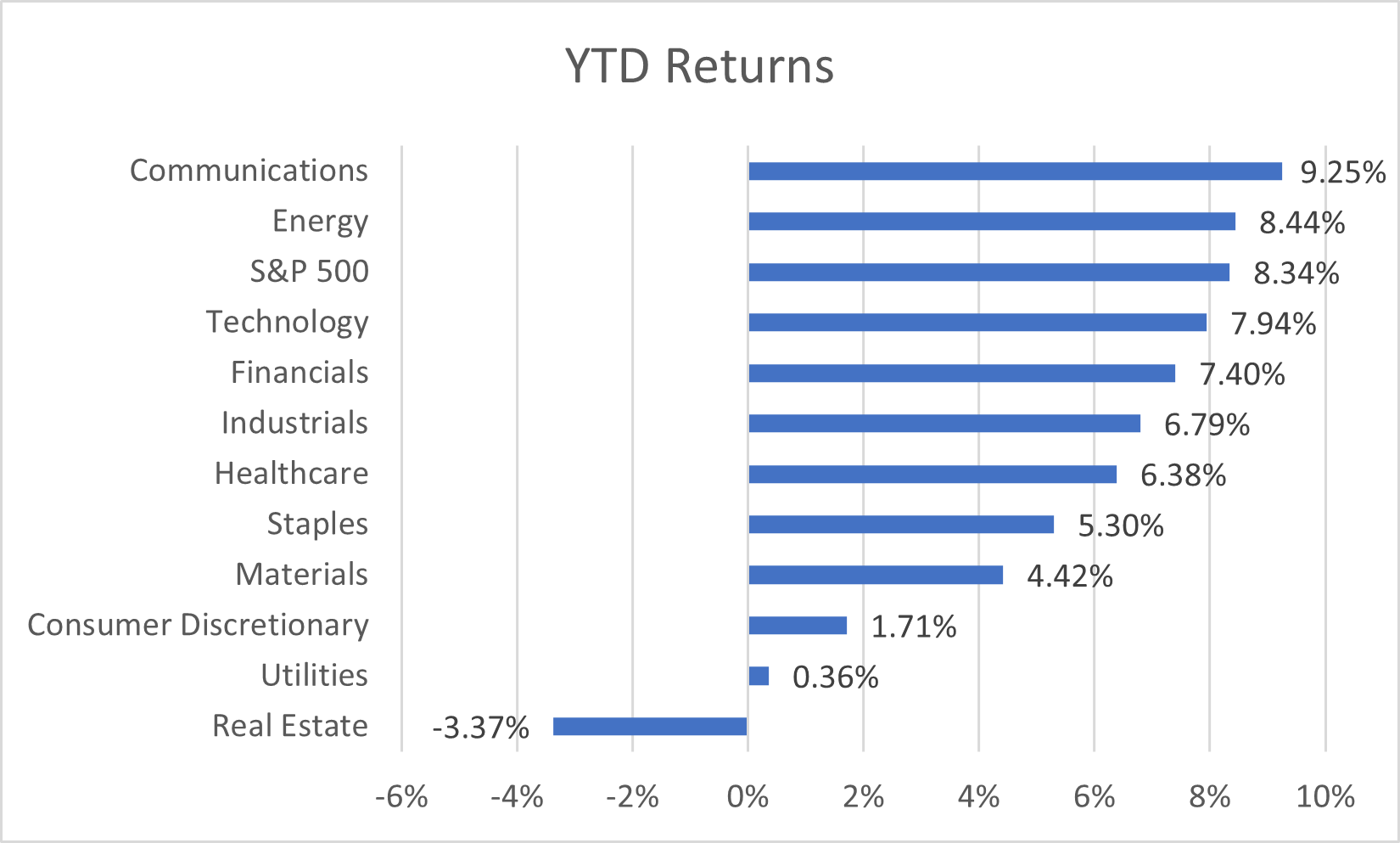

We are seeing gold and bitcoin prices soar potentially suggesting the inflation is here to stay for longer. The interest rate sensitive sectors of the market such as real estate and utilities are significantly underperforming the rest of the market.

While a recession is not fully averted at this time, we are yet to see if a recession is imminent. We do not see any signs of slowing in the economy yet. The market PE multiple is above 20 and the valuation seems a bit stretched.

Broad Indicators

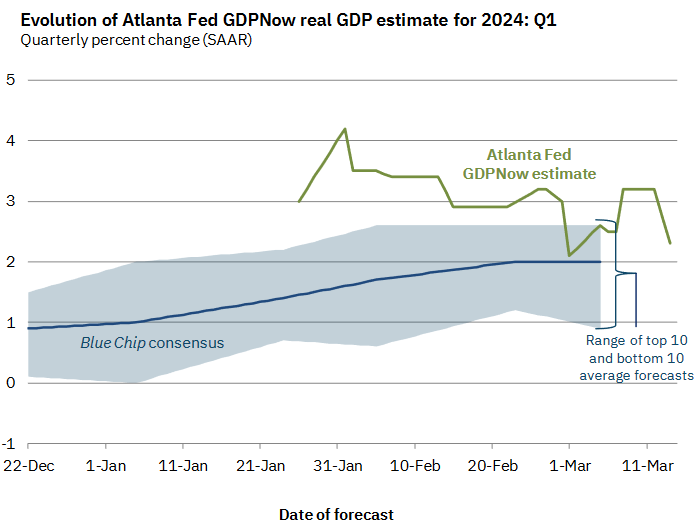

Atlanta GDP NowCast

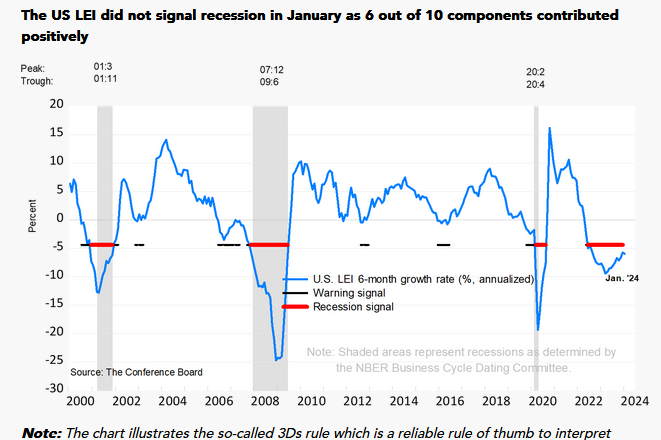

Conference Board's Leading Economic Indicator

US Dollar Index

Commodities

Gold

Bitcoin

Inflation

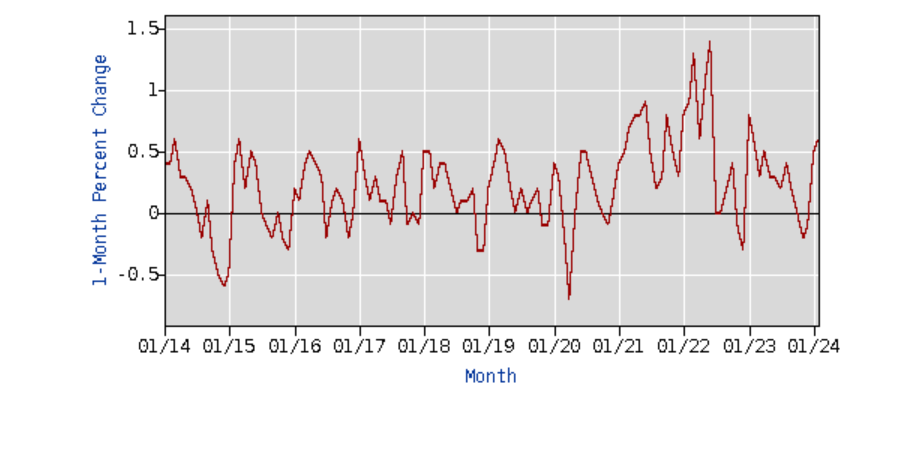

CPI Month over Month

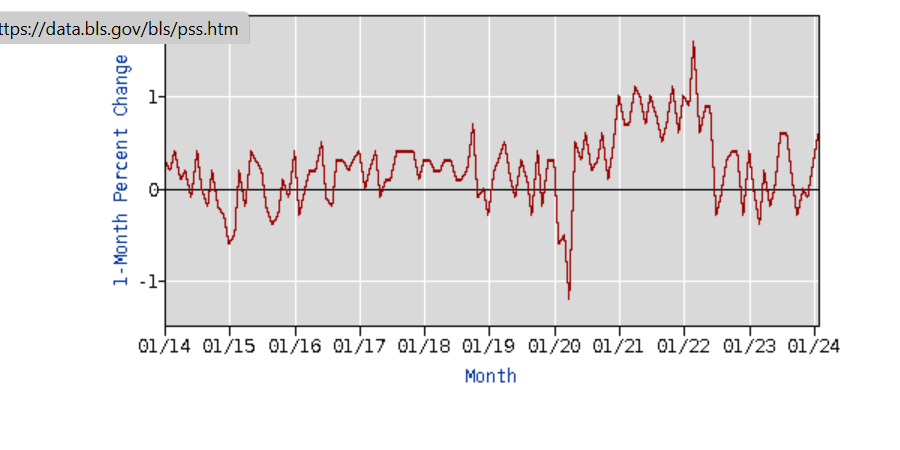

PPI Month over Month

Reported Year over Year Inflation Rate

CPI Components

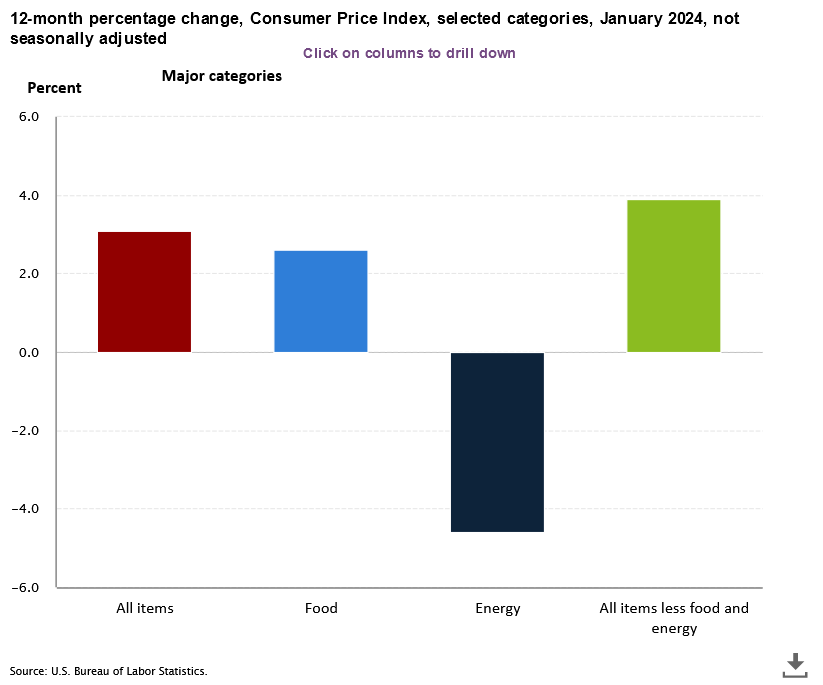

CPI Components Last Month

Source BLS.gov Consumer Price Index

CPI Components Last Month

Source BLS.gov Consumer Price Index

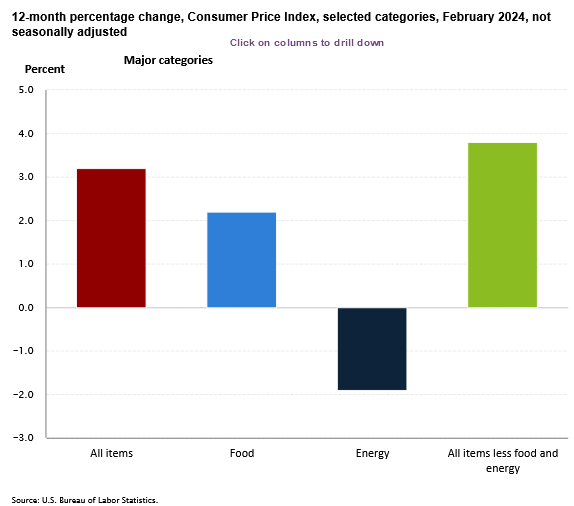

CPI Components This Month

CPI Components This MonthThe contributors to inflation have remained fairly consistent. However, the change in contribution from energy is noticeable this month. (Please note that the y-axis in both the graphs have different scales).

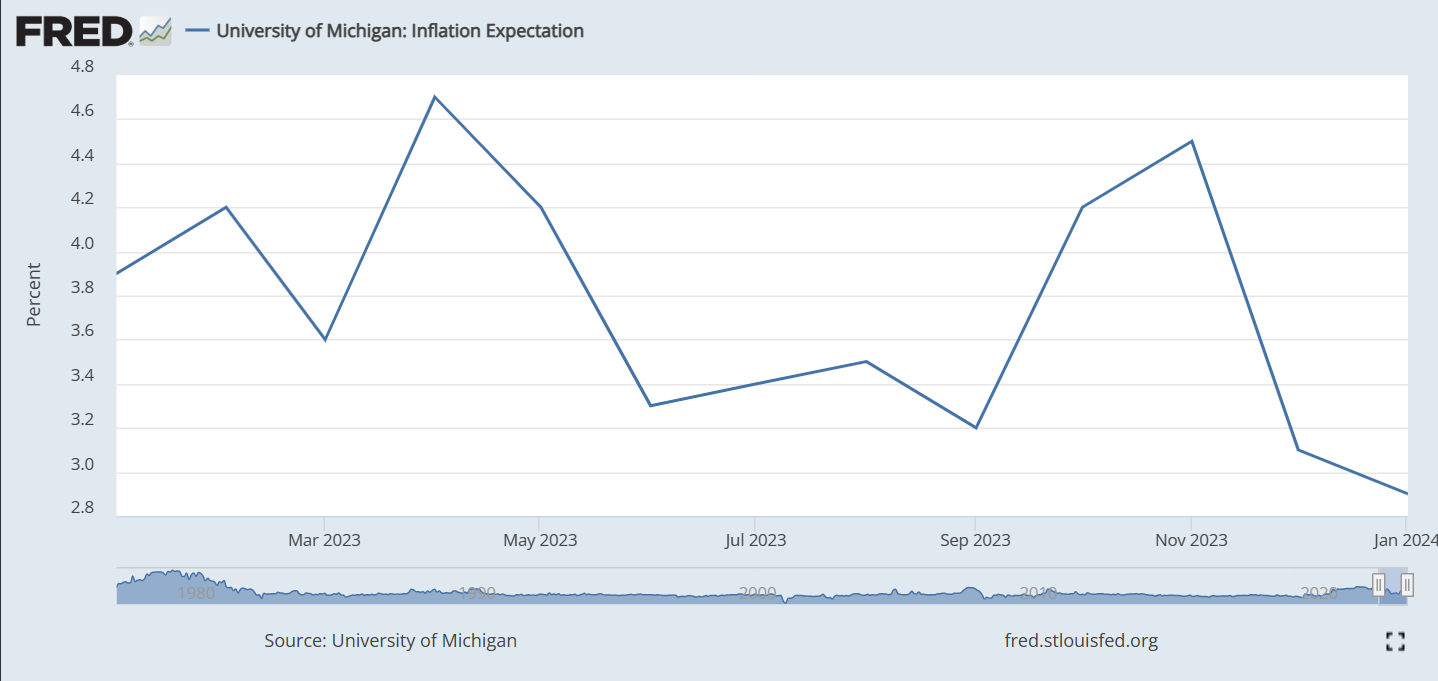

One Year Inflation Expectations

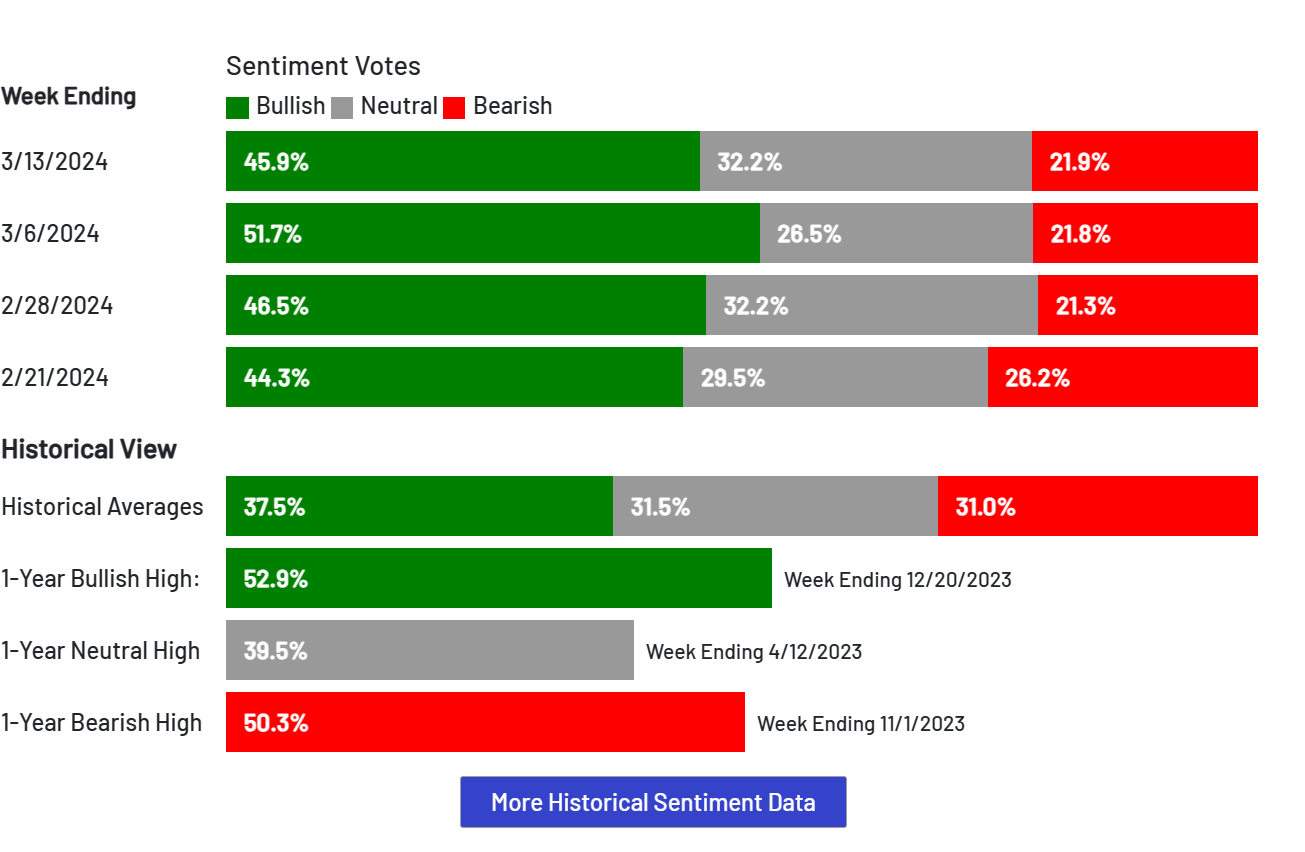

Sentiments

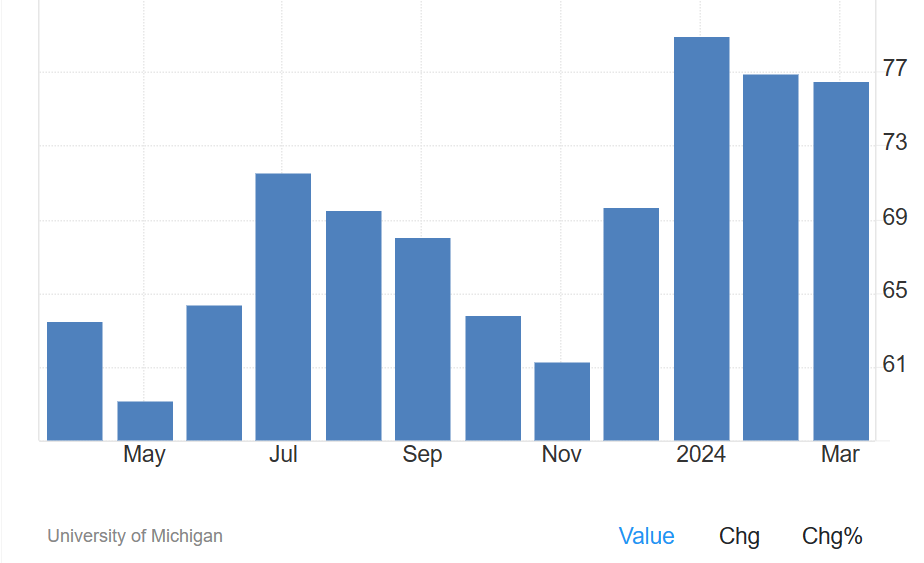

Consumer Sentiments

Investor Sentiments

The AAII sentiment has remained consistently bullish even after four months of run up in the S&P 500.

GDP Factors

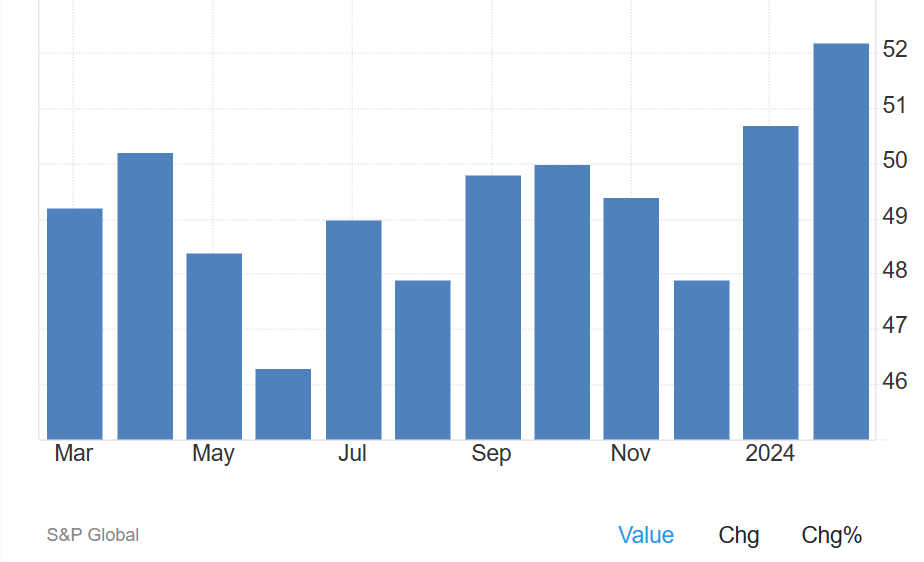

Manufacturing PMI

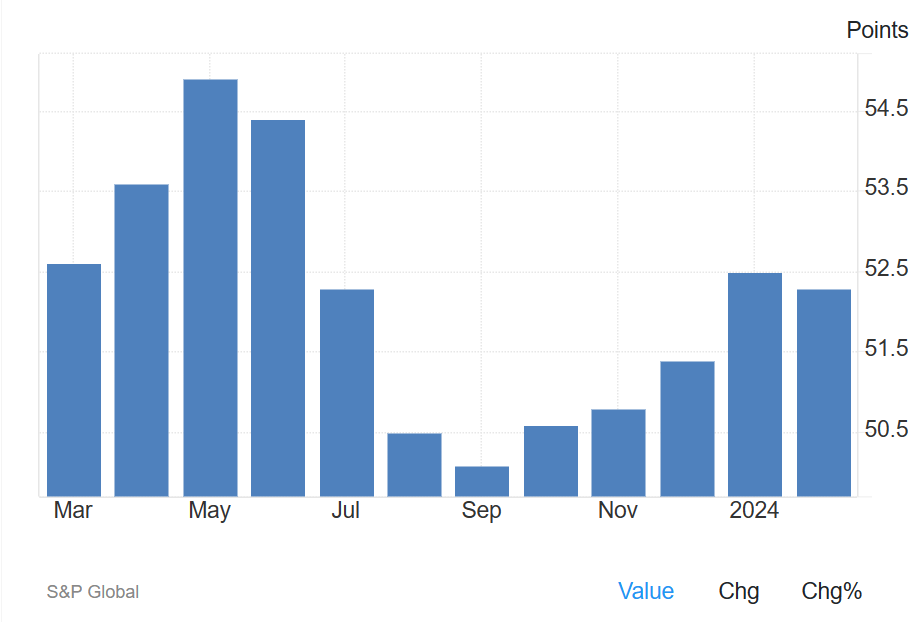

Services PMI

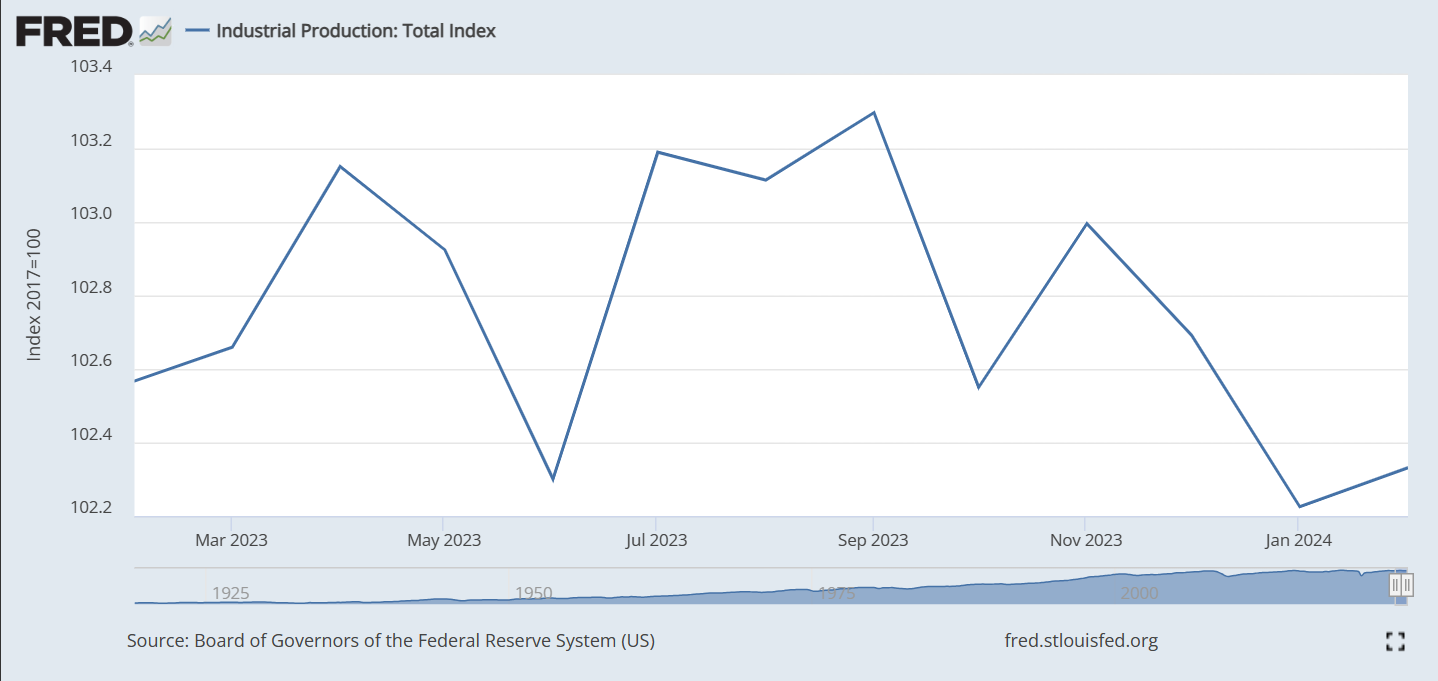

Industrial Production

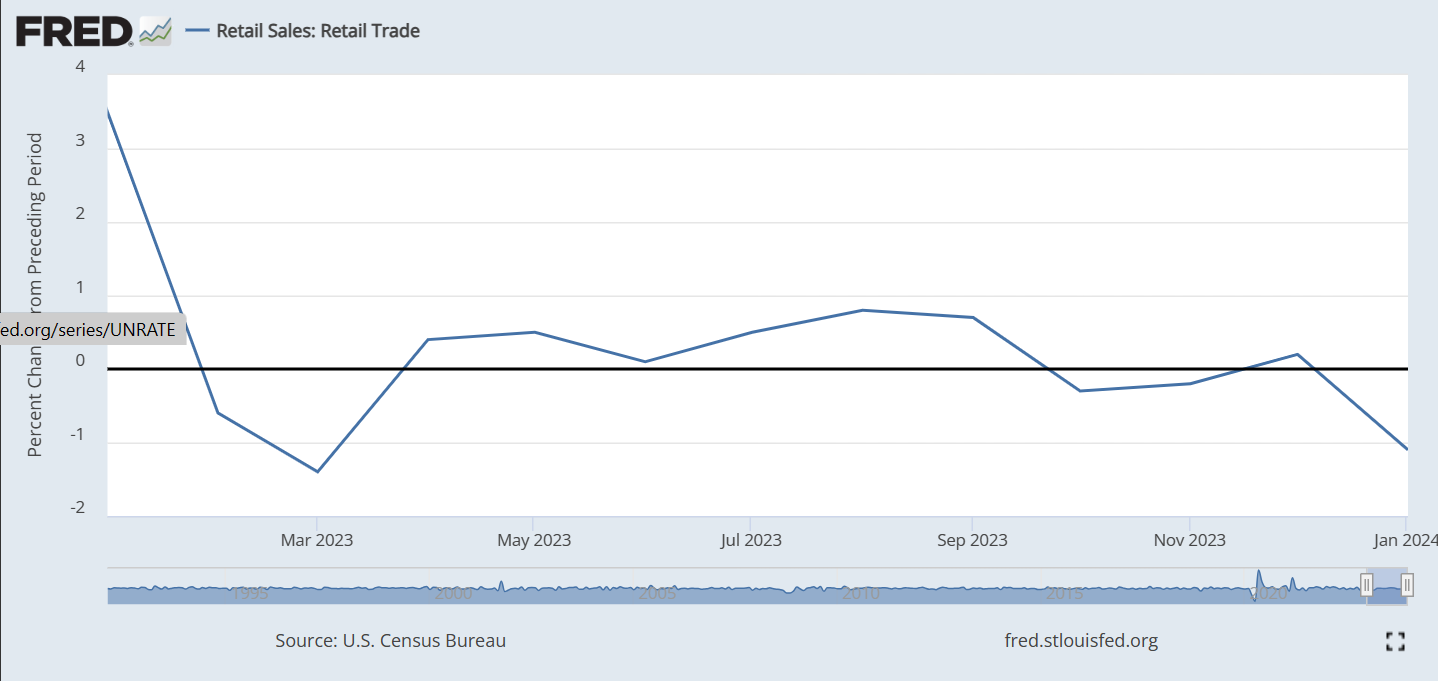

Retail Sales

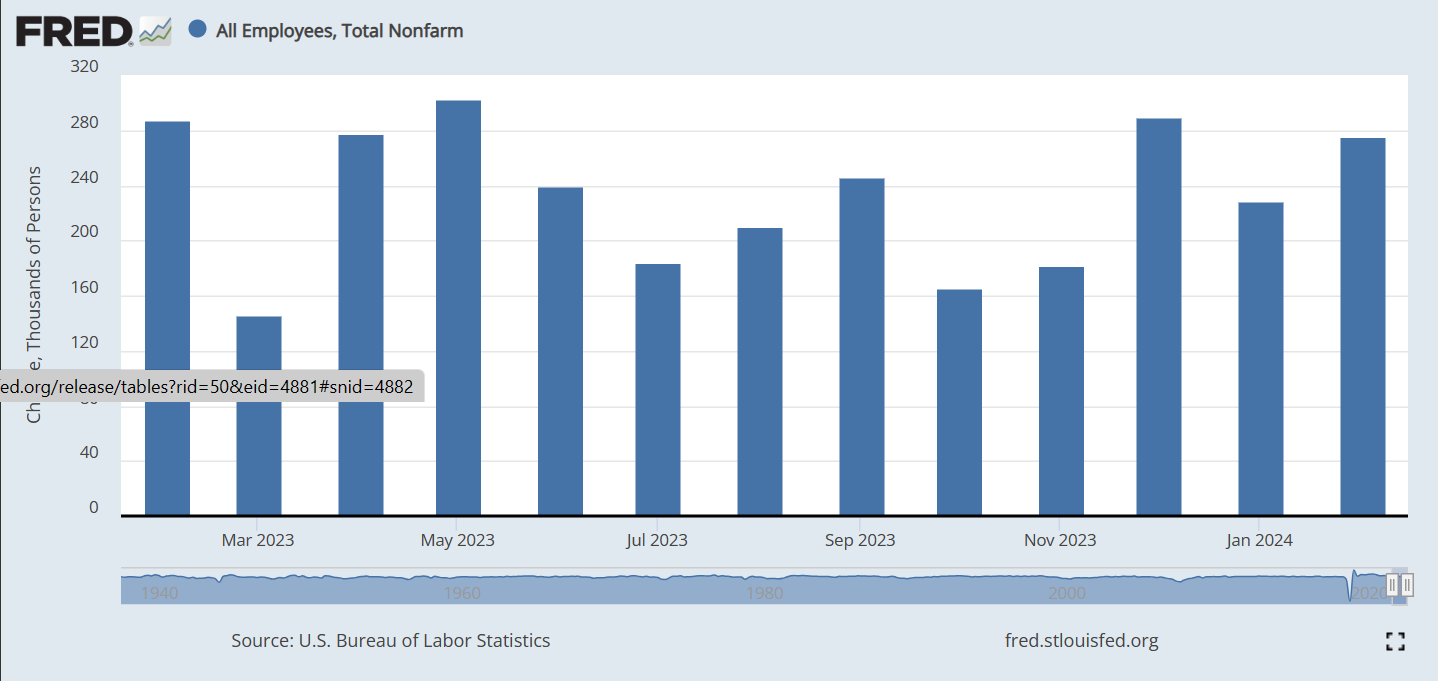

Non-farm Payrolls

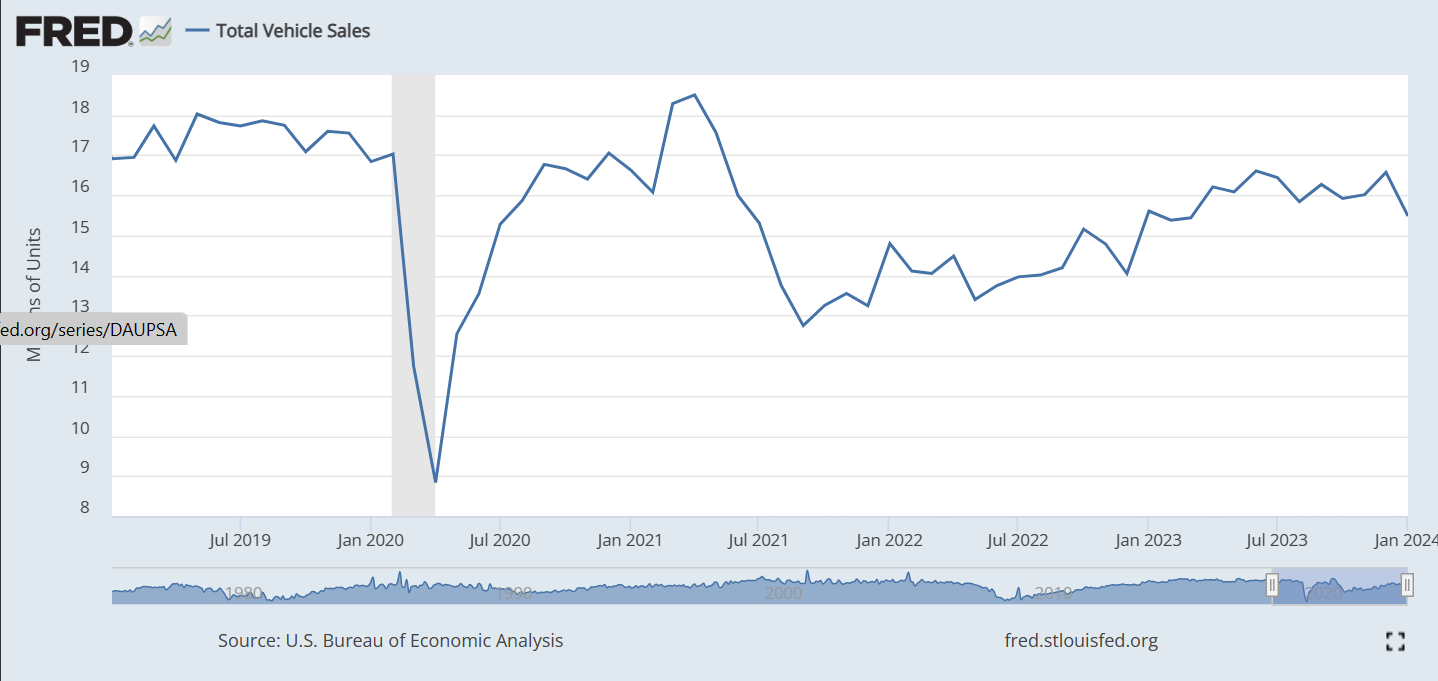

Total Vehicle Sales

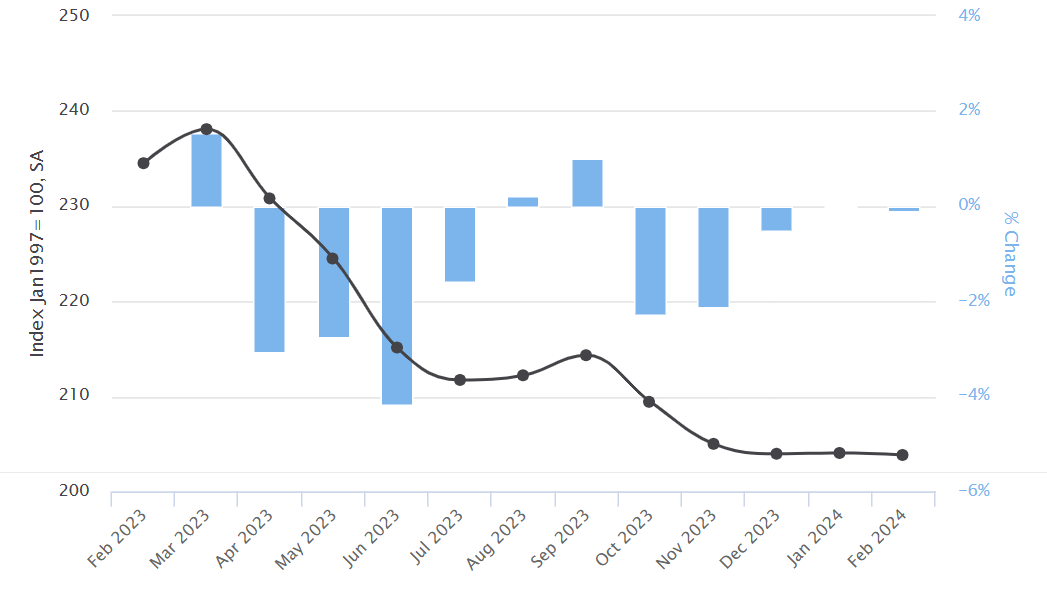

Manheim Used Car Index

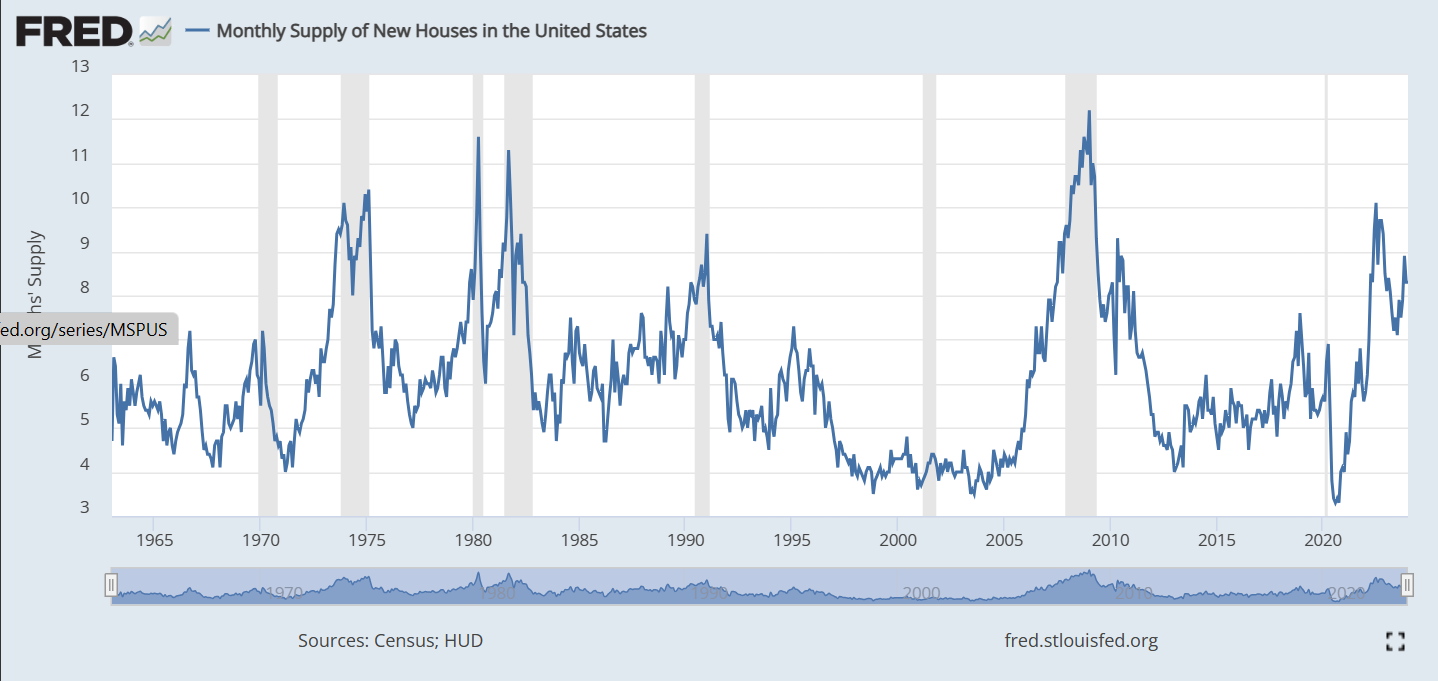

US New Home Sales

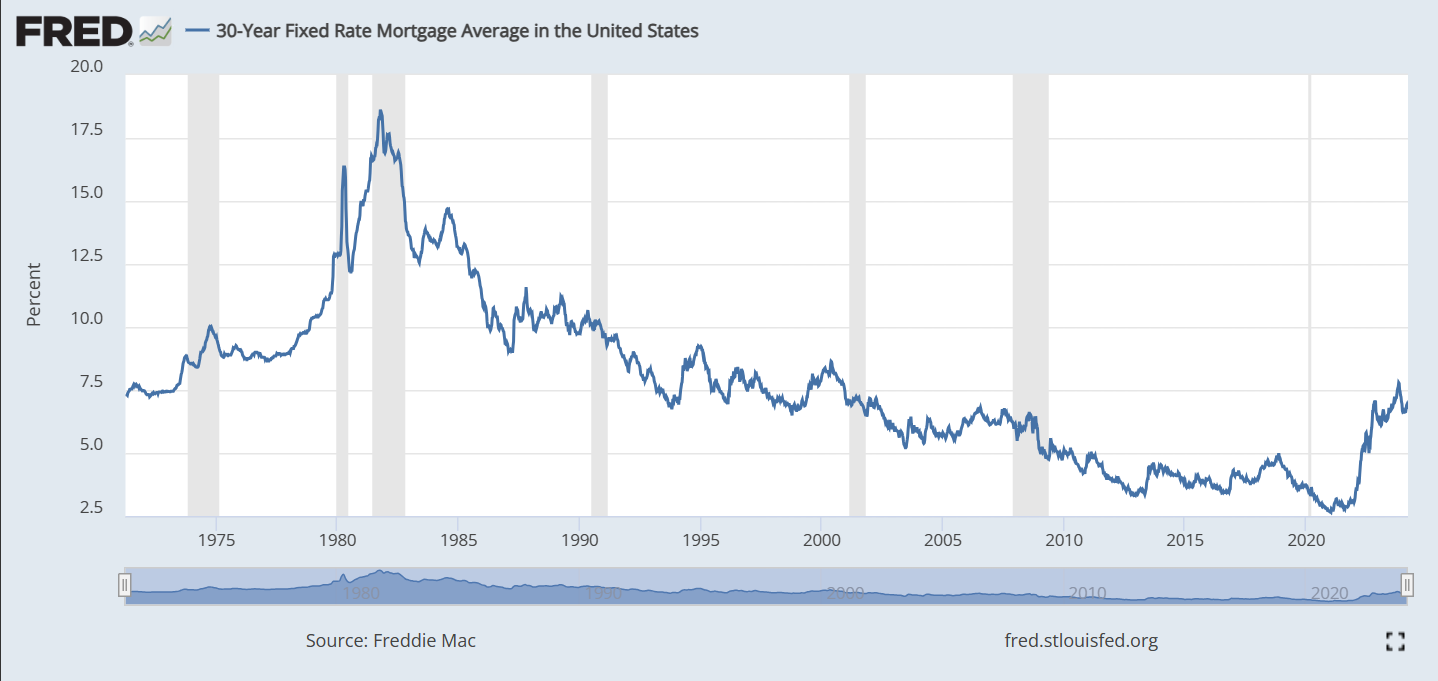

30 Year Fixed Mortgage Rates

The mortgage rates have followed the 10-year Treasury yield higher over the last few months. Recently as the inflation is contained and 10-year Treasury yield has rolled over, the mortgage rates has come down a tad bit.

Employment Indicators

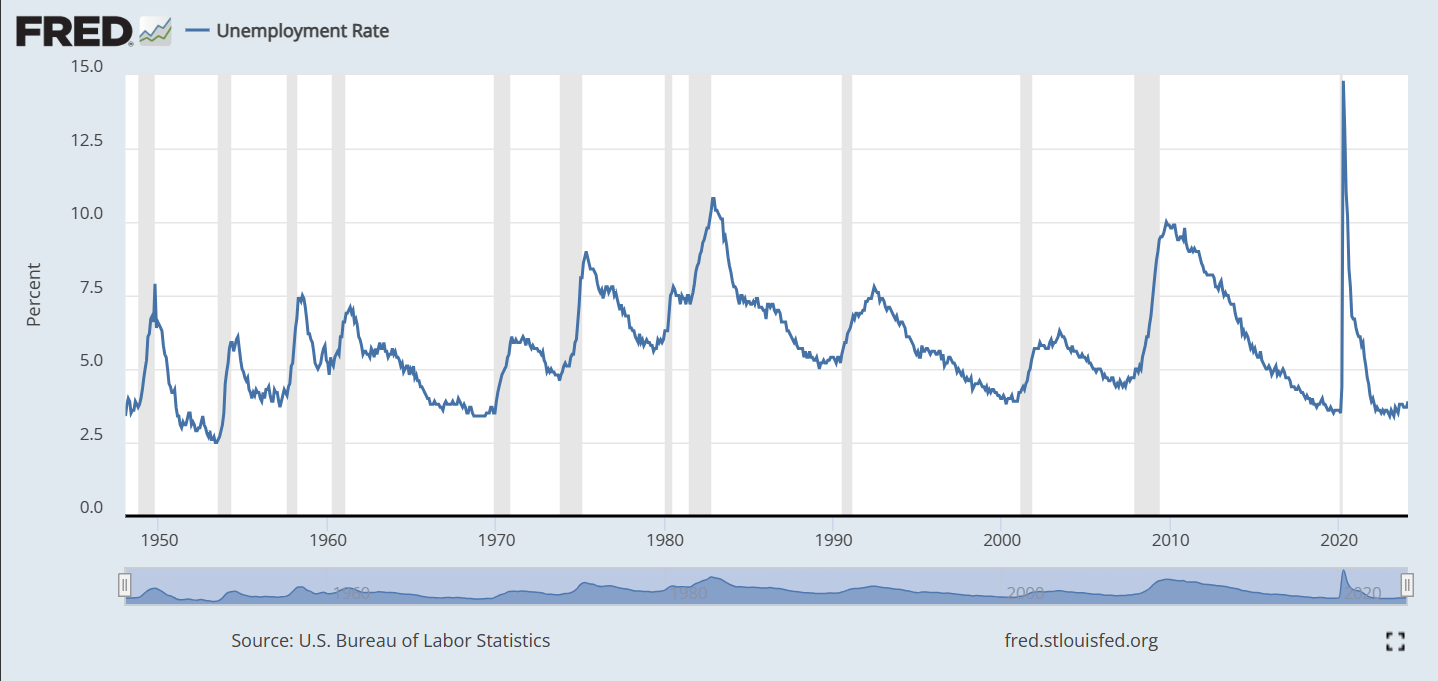

Historical Unemployment Rate

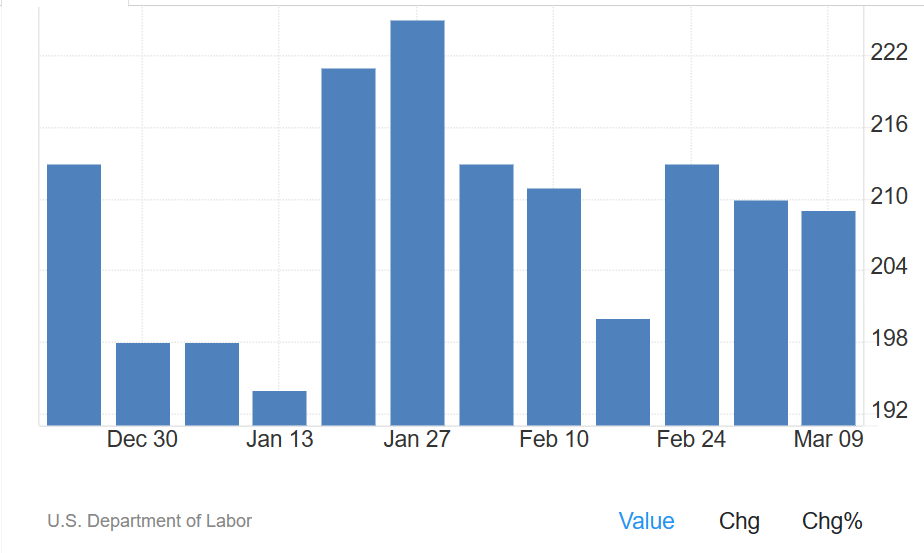

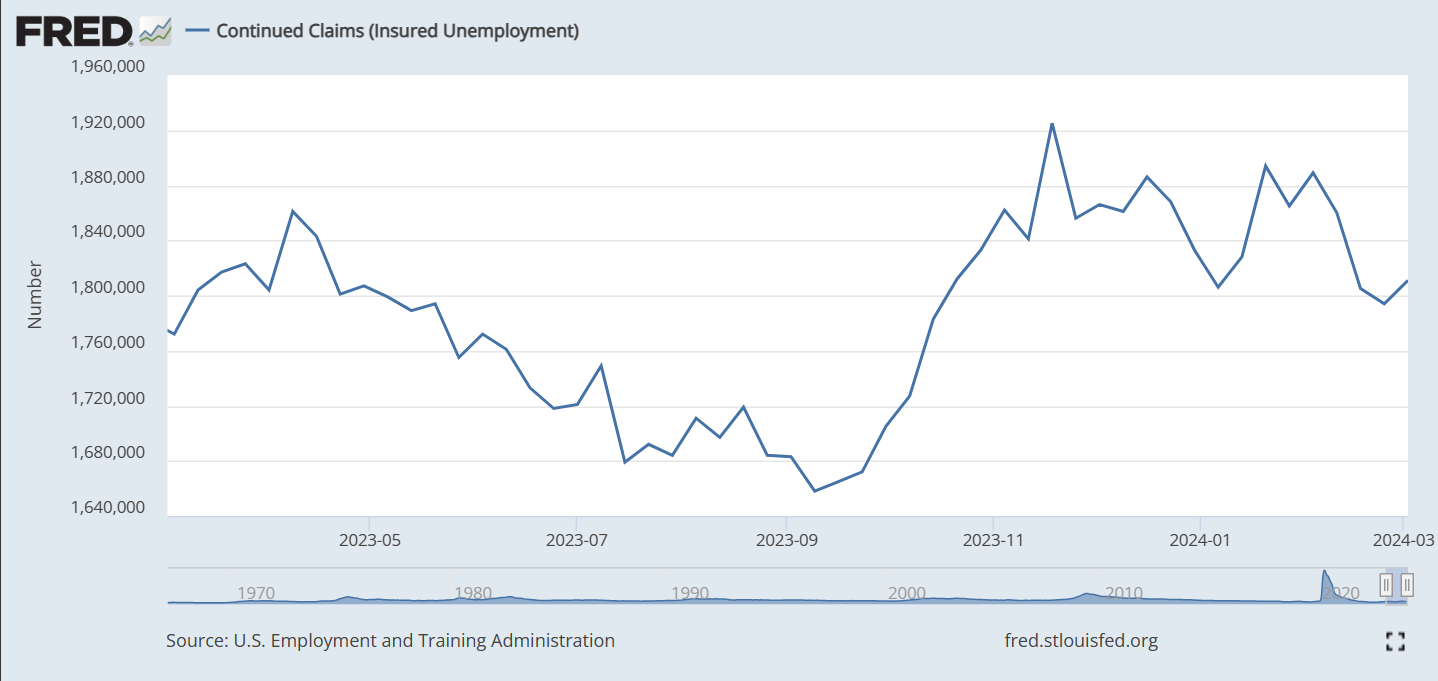

US Jobless Claims

This chart will be the first indicator of a telltale sign that unemployment is increasing. As you see the continuing

jobless claims number rise, it implies the people who lost their jobs are not going back to labor force fast enough

and the unemployment rate is starting to creep higher. Over the last couple of weeks, it has trended lower, indicating

a strong job market. It could turn out to be seasonal and it needs to be watched over the next few months if the continuing

claims build up.

This chart will be the first indicator of a telltale sign that unemployment is increasing. As you see the continuing

jobless claims number rise, it implies the people who lost their jobs are not going back to labor force fast enough

and the unemployment rate is starting to creep higher. Over the last couple of weeks, it has trended lower, indicating

a strong job market. It could turn out to be seasonal and it needs to be watched over the next few months if the continuing

claims build up.

Wage Growth Tracker

Market Indicators

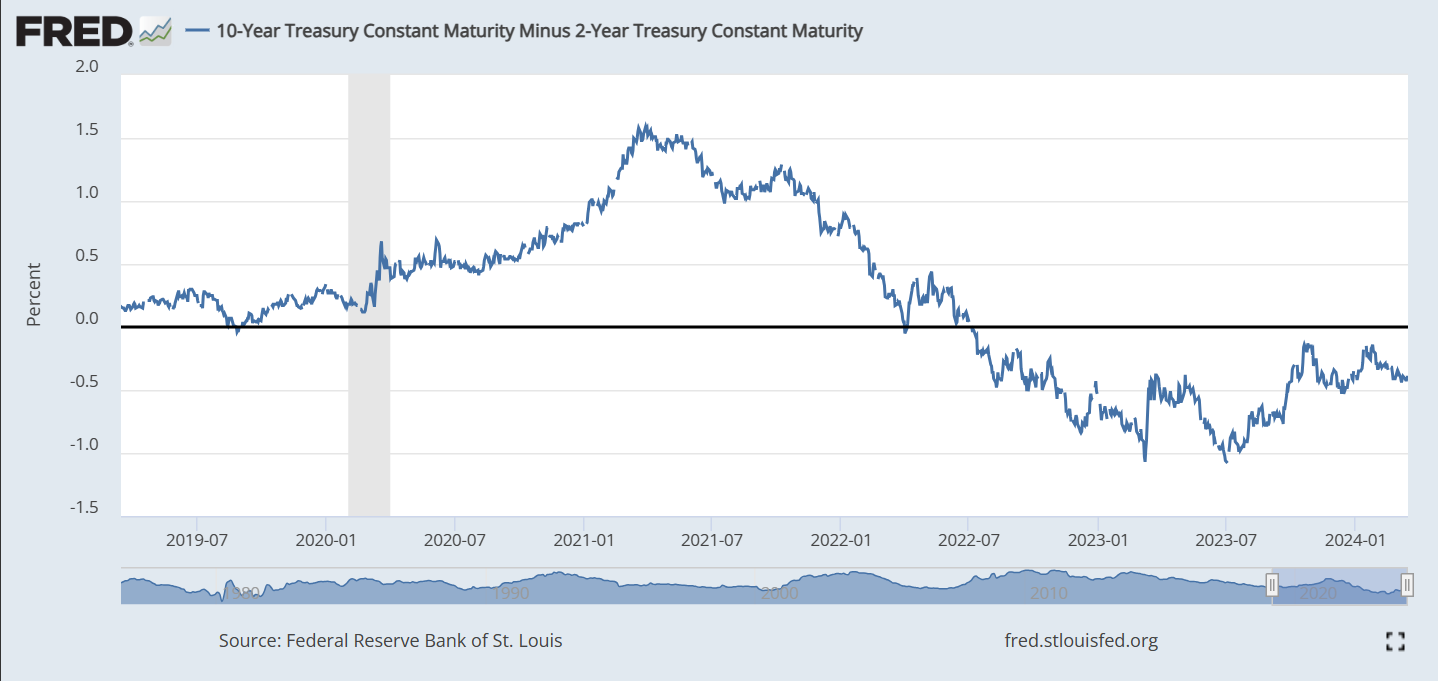

Yield Curve Inversion

Yield Curve - then and now

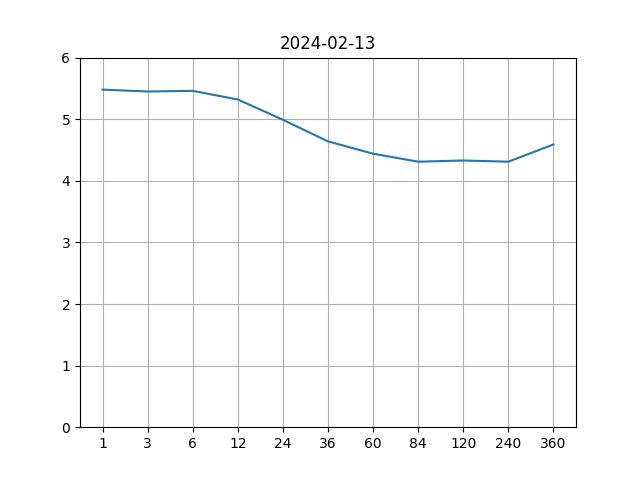

Yield curve - Then

Yield curve - Then

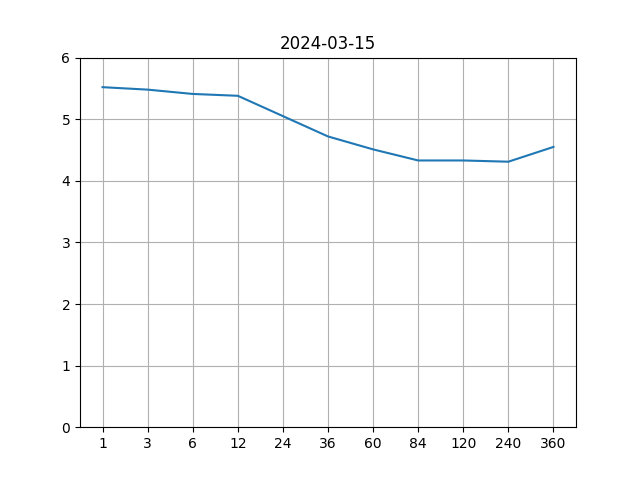

Yield curve - Now

Yield curve - Now Notice how the 1 year part of the curve has steepened a bit. Otherwise, the curve looks fairly identical to the curve one month ago.

Market Sectors

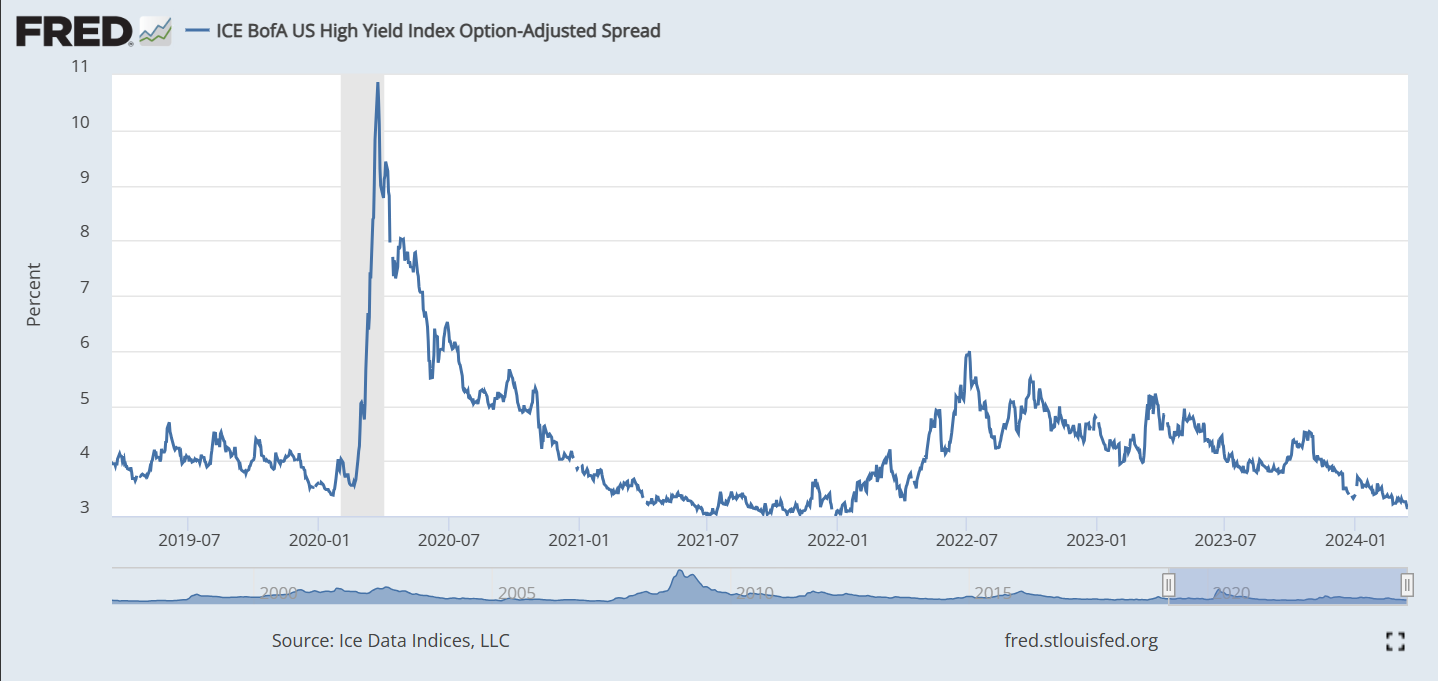

High Yield Index Options-Adjusted Spread

If the economy were to enter a recession, it is likely that some of the companies will struggle to keep up with their debt payments causing their credit spread to widen. This indicator shows how the credit spreads have been behaving so far.

The tight spread indicate that the soft landing narrative is actually playing out.

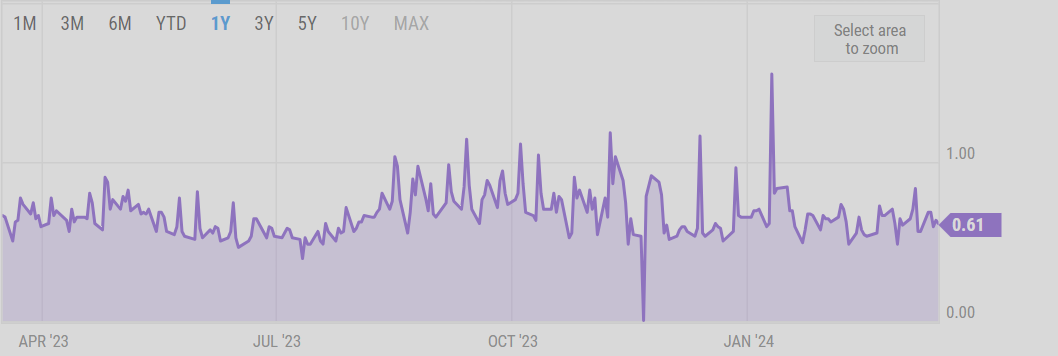

Put Call Ratio

A spike in put / call ratio indicates that investors are very apprehensive about a sudden fall in the equity markets. In January/February, we have not seen any interesting activities.

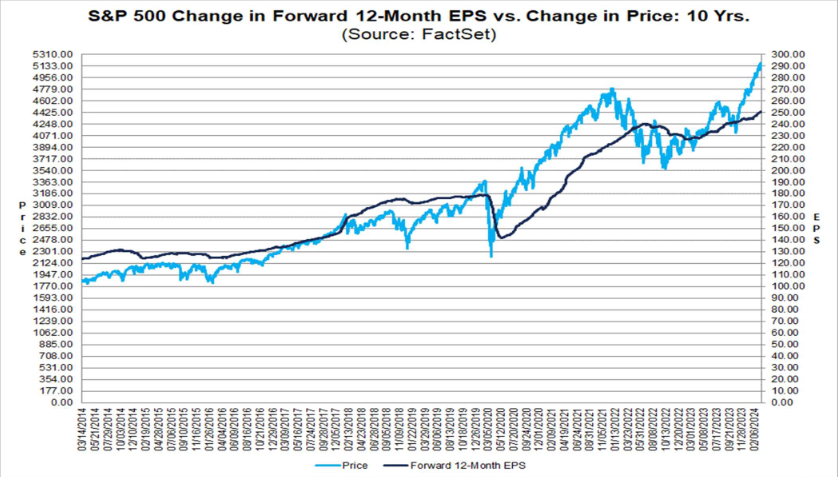

S&P 500 Current Valuations

The current earnings forecast by equity analysts estimate the earnings potential for S&P 500 companies to be around $250 which translates to a price to earnings ratio of 20.5 at the current S&P 500 price level. This is above the 5 year and the 10 year averages. The market is looking pricier by the day.

Diclosures

- Trillium Square Advisors LLC is a registered investment adviser offering advisory services in the state of North Carolina and in other jurisdictions where exempted. Registration as an investment adviser does not imply a certain level of skill or training, and the content of this communication has not been approved or verified by the United States Security and Exchange Commission or by any state securities authority.

- Information presented is for educational purposes only and does not intend to make an offer or solicitation for the sale or purchase of any specific securities, investments or investment strategies. Market data, articles and other content in this presentation are based on generally available information and are believed to be reliable. Trillium Square does not guarantee the accuracy of the information contained in this presentation. The information is of a general nature and should not be construed as investment advice and relied upon in making investment decisions.

- Investments involve risk and are never guaranteed. Be sure to first consult with a qualified financial adviser before implementing any strategies discussed herein.

- Past performance is not indicative of future performance.

- The content of this communication and any accompanying documents are not to be copied, excerpted or distributed without express written permission of the firm. Any other use beyond its author’s intent, distribution or copying of the contents of this presentation is strictly prohibited. Nothing in this document is intended to be legal, accounting, or tax advise, and is for informational purposes only.

- Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. In fact, there are frequently sharp differences between hypothetical performance results and the actual results subsequently achieved by any particular investment strategy. Hypothetical performance for illustration purposes only.

- Trillium Square will provide all prospective clients with a copy of our current Form ADV, Part 2A (Disclosure Brochure) upon request. At anytime you can view our current Form ADV, Part 2A at https://adviserinfo.sec.gov