Summary

There has been a flurry of data updates and changes in January that are very much in contrast with the trajectory we have

been on for the few months prior. We are seeing a bounce in most of the economic data, bond yields and most surely in equity

prices. While this may all seem like good news, perhaps the apt metaphor to describe this could be the following:

- Kicking the recession can down the road.

- Inflation has been more sticky than anticipated.

- Soft landing Vs hard landing? Maybe there is no landing after all!

All these could be chalked up to the January effect - the optimism for the new year rises equity prices in January. But, it seems

more than that. The jobs market has confounded the consensus estimate and printed 500k+ payroll in January, more than double of

the consensus estimate.

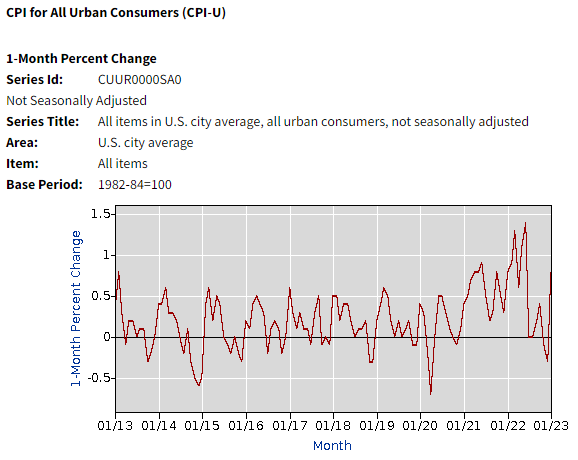

What is certain is that inflation is behaving as usual. It does not go down in a straight line. The print was 0.8% for January, highest

in the past few months. We only hope that it adheres to the declining trend in the coming months and does not provoke an aggressive FED. We

prefer a soft or no landing to a hard landing.

Looking at a glass half empty, FED's actions are effective with long and variable lags. By the time the results of their actions are

finally here, I hope the current optimism does not push them to act so hawkishly that we end up in a deep recession. The story from the

rest of world confirms softening macroeconomic data as Lakshman Achuthan from ECRI points out in his recent macrovoices podcast interview.

Broad Indicators

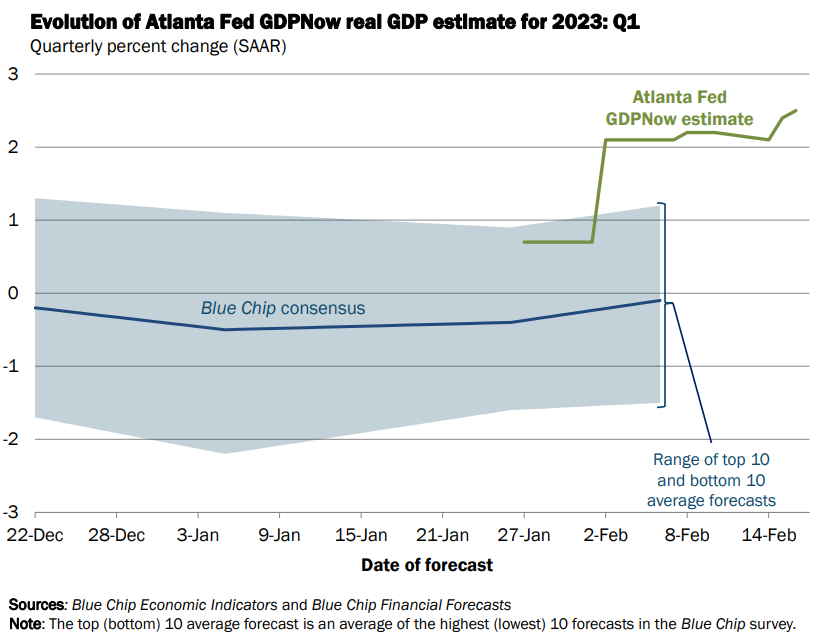

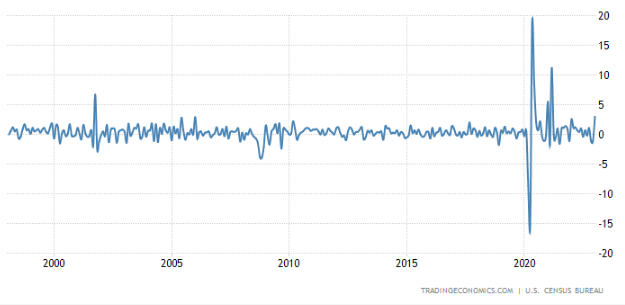

GDP is currently projected to be 2+% for Q1 2023. The positive GDP number is primarily due to the consumer

still being strong as seen in retail sales number and an even healthier employment figure.

Since the last Fed press conference and especially after the very good payroll numbers at the start of February, the Dollar

index has started to climb again. The CPI number has come in hot, further increasing the chances for rate hikes to continue.

Commodities have generally been easing over the last few months. The rise in Dollar is

a negative for commodities. Also, if there is demand destruction due to an impending

recession, it does not bode well for continued demand for commodities.

Gold's positive momentum has faded as the dollar has started to climb.

BitCoin has diverged from other macro assets such as gold and the dollar this month. In spite of the climb

in the dollar, BitCoin has held up and even seen rising!

Inflation

In the month of January, inflation climbed by 0.8%. That is the largest climb since last June. Blame it on

the seasonality or January effect. This certainly gets FED's attention to keep things tighter for longer.

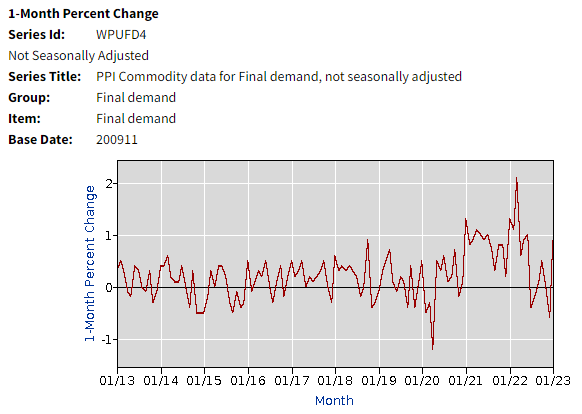

The pop in CPI is also reflected in a pop in the PPI and the expected change for the month of January is around 0.9%.

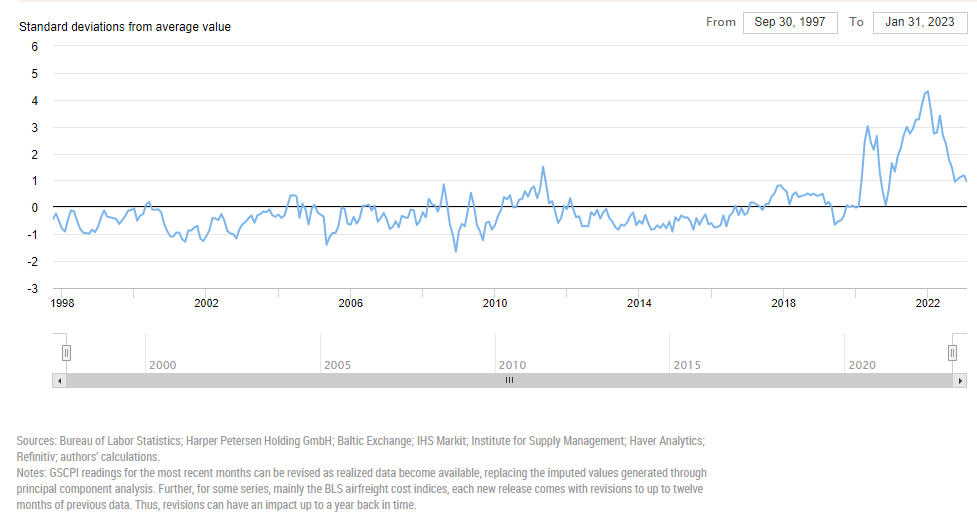

If you believe the rise in inflation was transitory, here is a comforting chart. Many believe the cause

of inflation was due to supply side constraints caused by COVID shutdowns across the world. This chart tracks

the pressure on global supply chain. Clearly, according to this data, the pressures have been coming down and are

now close to 1

of the normal pressure.

This chart has not meaningfully deviated in the light of the higher inflation in the month of January. Perhaps

there are other reasons for inflation - such as de-globalization, runaway growth in the US economy due to the fiscal stimulas in 2020.

The exact reason will be very clear in hindsight.

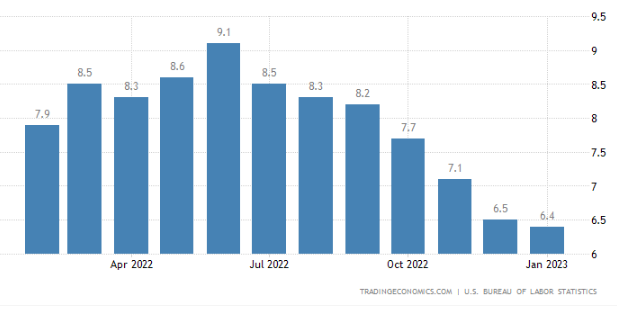

This is the headline inflation number that everyone talks about. Currently, for January 2023 we are at 6.4%. Inflation is

known to be sticky. The current trajectory is still promising and there is no need to give up hope yet.

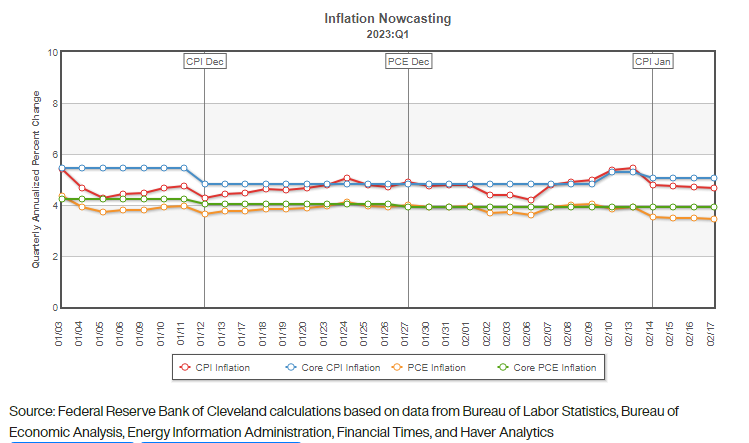

Inflation Nowcast is built using other economic indicators besides the Inflation report to come up with the latest CPI number.

Thus, it gives a more up-to-date picture on what the CPI is at any given time. Per the Nowcast, it is interesting

to see that headline CPI has gone below core CPI indicating the cooling in gas and food prices while the core part of the inflation

has remained fairly sticky.

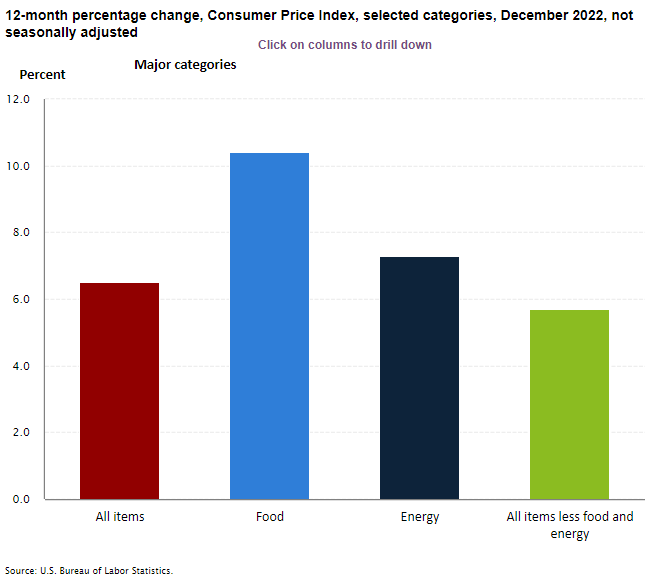

CPI Components Last Month

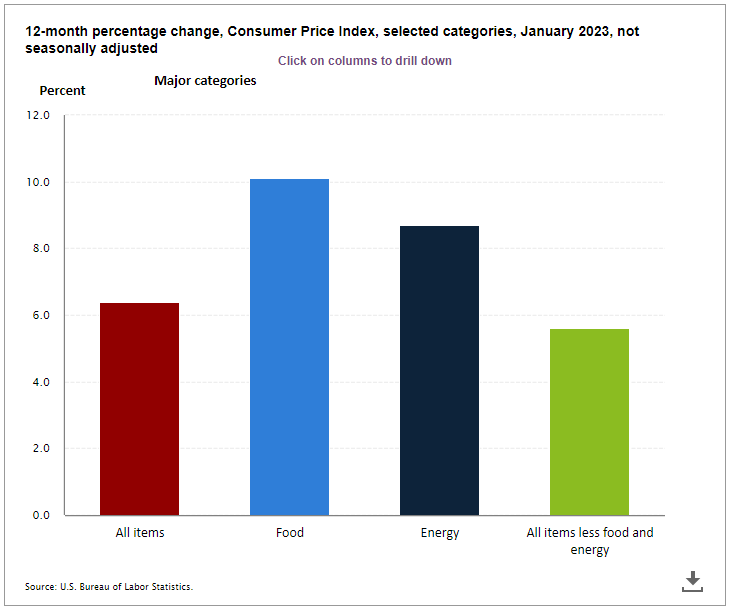

CPI Components This Month

Food inflation has markedly come down this month compared to the last, while energy has marginally gone up.

(Please note that the y-axis in both the graphs have different scales).

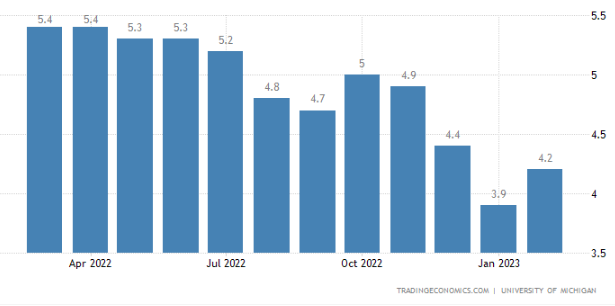

This survey data shows that inflation one year from now is expected to be 4.2%.

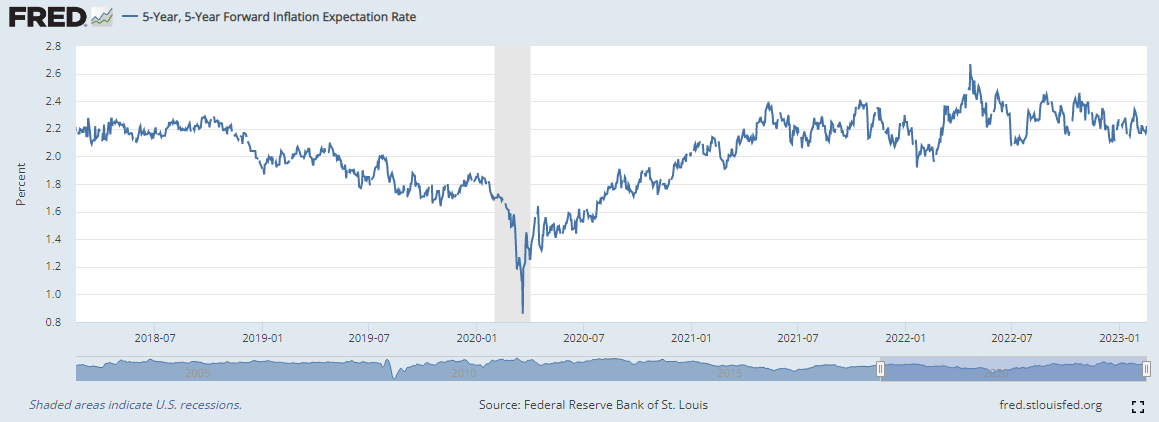

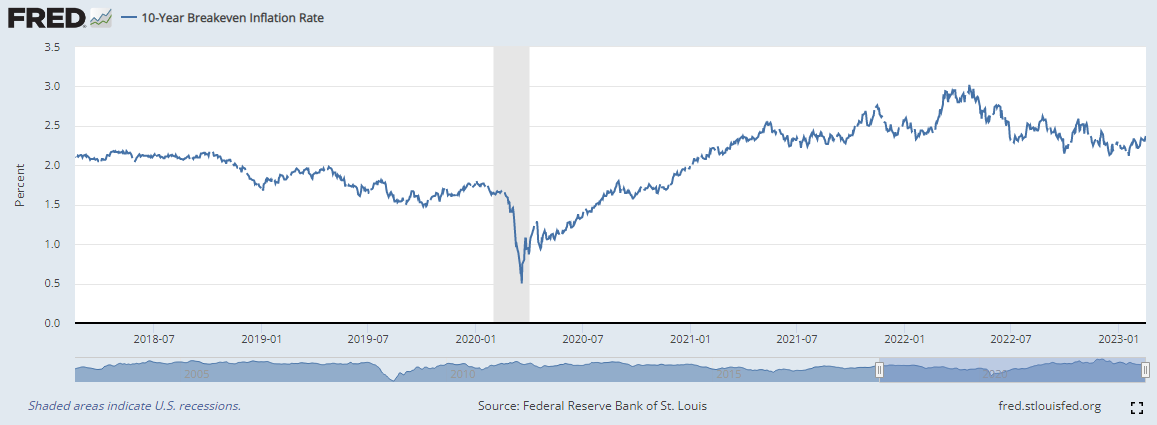

This is a market based indicator showing the inflation in 5 year forward interest rate, 5 years, is in a 2

handleIf a measure such as stock price ranges in 35.01 through 35.99, the stock price is said to have a handle of 35.

.

This indicates the current inflation bout is just a blip in the radar and not an indicative of a structural change in the

economy.

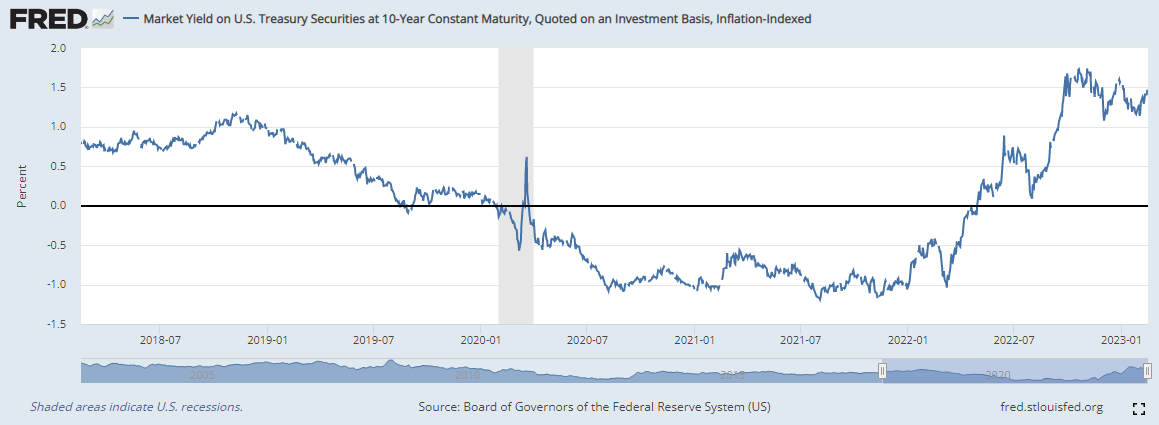

This is another market based indicator showing the inflation 10 years from now is in a 2

handleIf a measure such as stock price ranges in 35.01 through 35.99, the stock price is said to have a handle of 35.

.

This indicates the current inflation bout is just a blip in the radar and not an indicative of a structural change in the economy.

It is great to see real yields in the positive territory after a long period of being on the negative side.

This indicates the optimism in bonds where you can make some positive

carryYield on the investment.

.

Sentiments

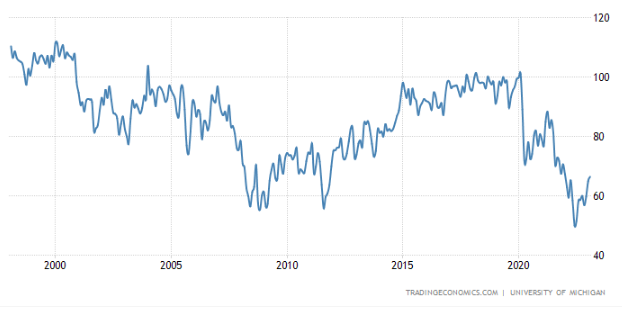

The survey indicator for consumer sentiments continues to leap upwards in January! While this is a good sign,

it could also be due to the holiday effect. Also, we would like it come above 80 to confirm everything

is great in consumer land.

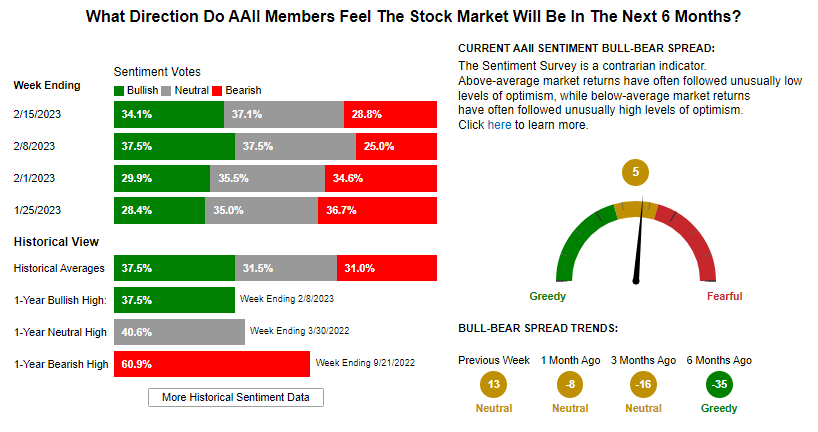

The investors have remained bearish for a while. Investors are getting bullish on the margins with the New Year. S&P is

above its 200 day moving average as we write and this may ebb their bullishness.

GDP Factors

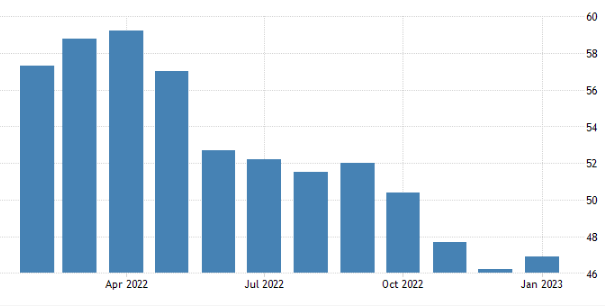

Manufacturing PMI reading indicates a contraction (below 50) which is not great and does not share the Atlanta

FED optimism on GDP growth. More so, this may indicate the slowdown in the economy that is yet to come. However,

this month, we are seeing a bump to the positive side and we hope it builds up.

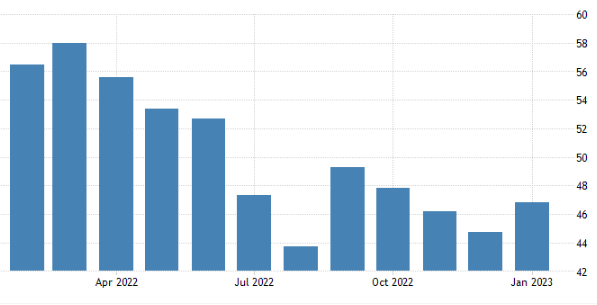

Services PMI reading is also in line with the Manufacturing PMI indicating a contraction. However, like the

Manufacturing PMI, we see the bump in the positive direction. Many are jumping to the conclusion that this may

indicate a soft or no landing scenario, essentially implying that we may avoid a recession.

Industrial Production is still positive but close to zero. We will take what positive indicators we can get and

be happy with it.

Retail Sales had a marked positive bump this month. Perhaps the after holiday sales is the cause. We hope that this positive

attitude continues in the coming months.

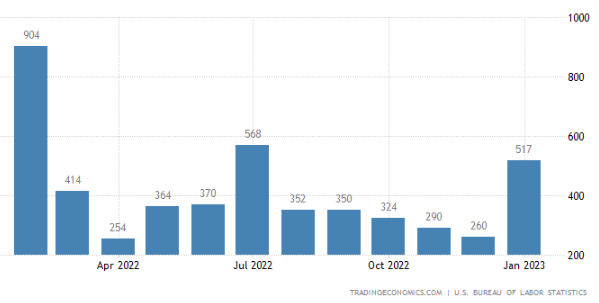

Non-farm payrolls have stubbornly been too good indicating economy is still adding jobs. This month, the jobs number broke

the consensus expectation by almost 100%. While there are layoffs taking place in Tech land, the economy quietly has been

adding so many jobs! If jobs are plenty and unemployment is record low, there can be no recession. This just makes FED's job

so much harder.

Total Vehicle sales inched higher this month making a short term trend upwards.

The used car prices are starting to inch up again seemingly the demand coming back up.

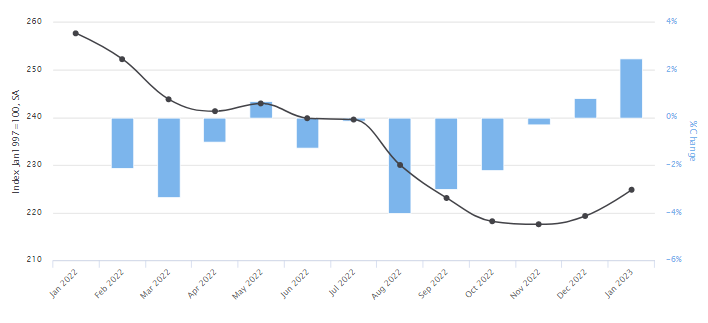

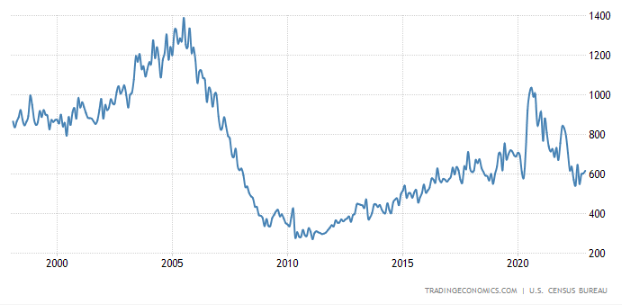

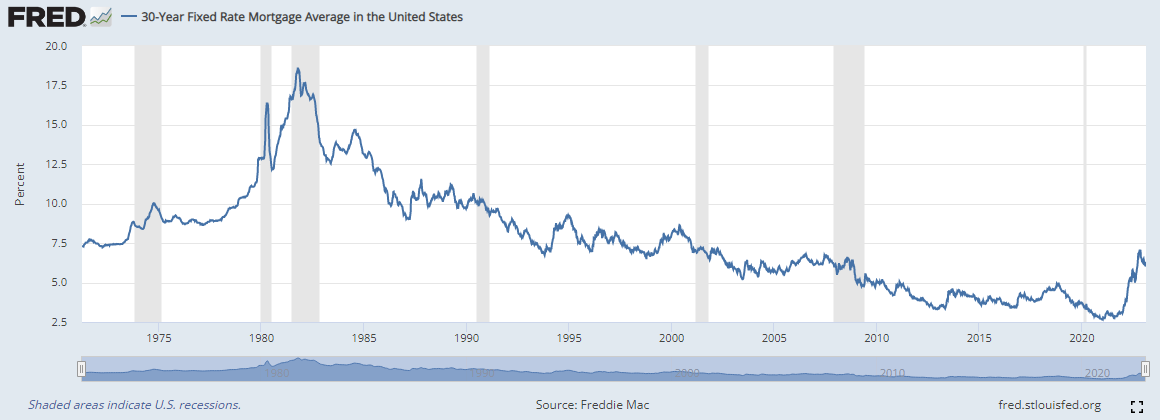

New home sales have followed the rise in mortgage rates and have been slowing considerably. Price corrections

are now seen in many key markets. Home buyers who financed at low rates will be reluctant to make any moves

as the rates have gone up considerably.

The mortgage rates are stabilizing and buyers have been coming back to the market. I hope the market thaws well this

spring and into the summer.

Employment Indicators

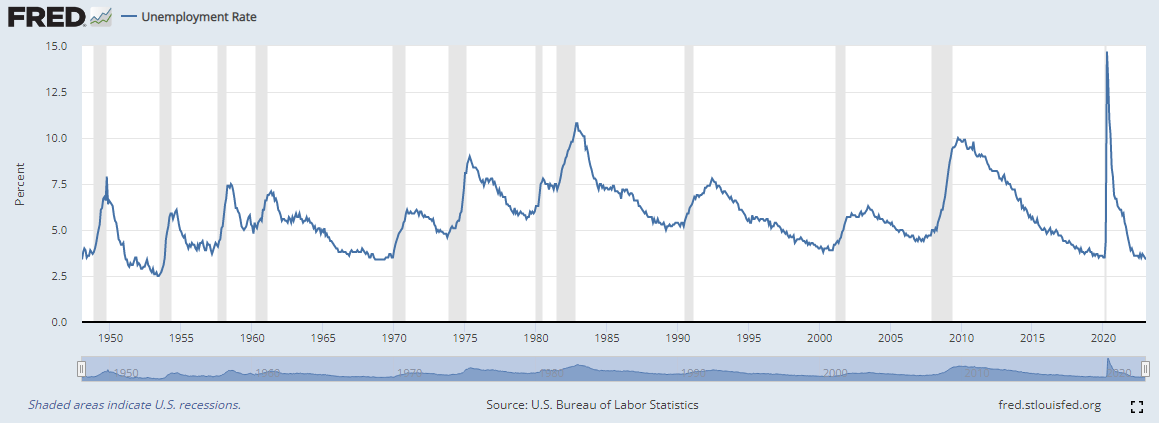

The unemployment rate has remained low despite the FED's attempt to induce a slowdown. This indicator is a lagging

indicator and we do expect to see this number creep up in the months to come.

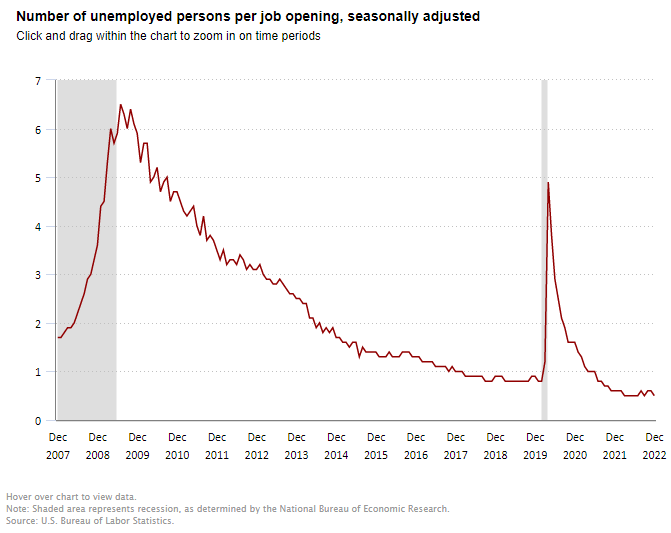

There are about 2 job openings for every unemployed person looking for a job.

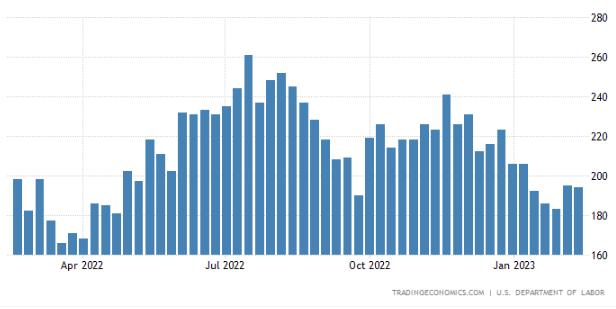

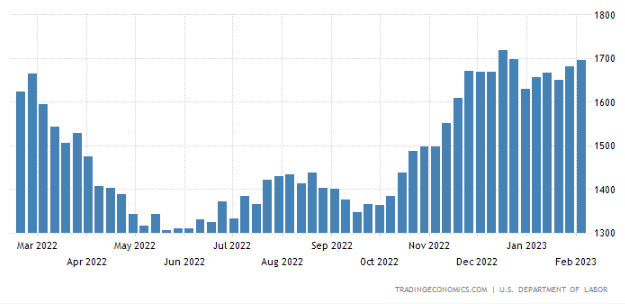

This chart will be the first indicator of a telltale sign that unemployment is increasing. As you see the continuing

jobless claims number rise, it implies the people who lost their jobs are not going back to labor force fast enough

and the unemployment rate is starting to creep higher.

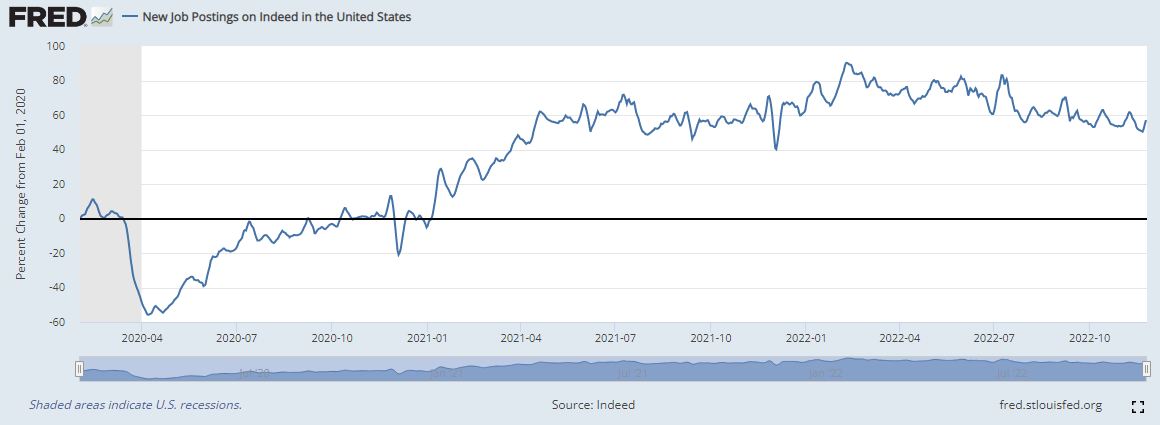

Interestingly, the rate of change in job postings is reducing but the total jobs are still rising according to

this indicator. While this is consistent with the BLS report on job openings to unemployed, we expect to see

some sharp corrections if a recession is imminent.

While wage inflation has followed inflation in goods and services, we are glad to see that the inflation has not

become endemic in the job market. The wage inflation rate at 6.1% still trails the overall headline inflation rate.

Market Indicators

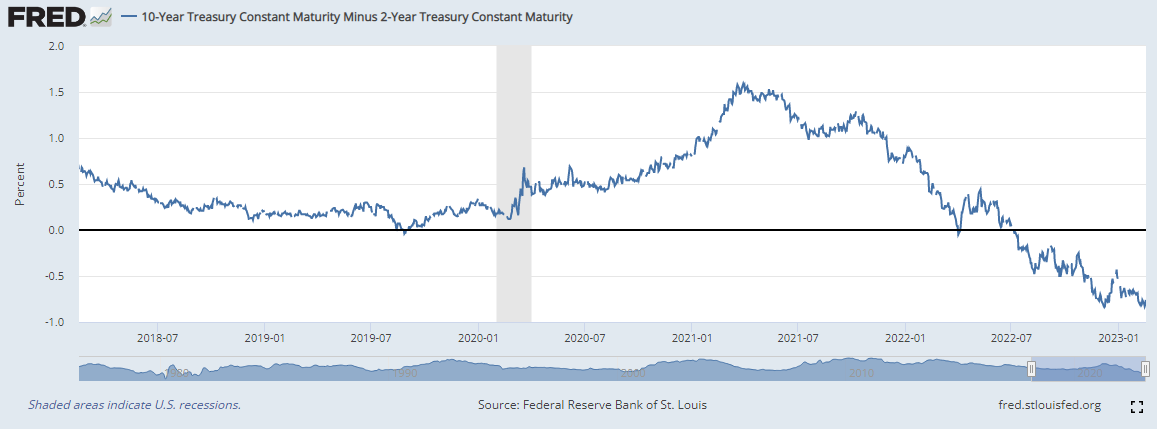

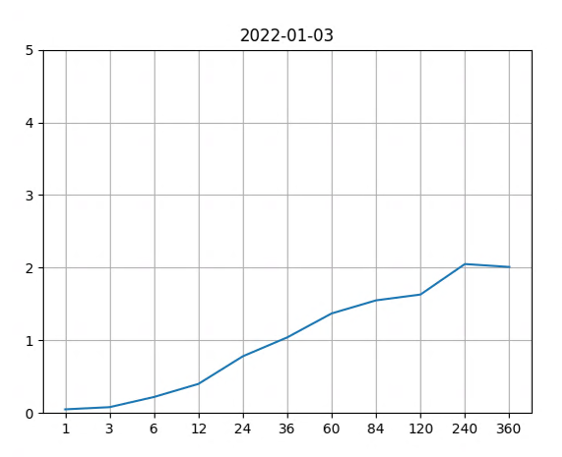

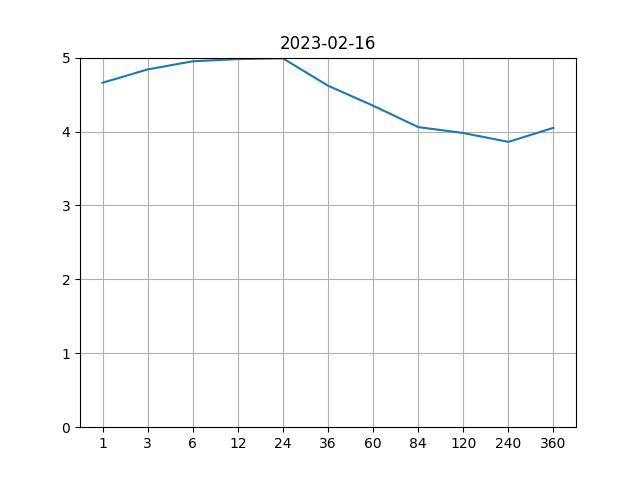

The yield curve remains inverted - the short end of the curve is above the long end of the curve. The inversion is

one of the largest in the last 40 years. This follows

the FED's aggressive actions to combat the 40 year high inflation rates. From a forward looking perspective, a yield

curve inversion is one of the strongest indicator for future recession.

There has been debate on whether the current recession prediction has the most consensus ever seen. If so, the recession

may not even come to a pass as everyone is expecting one. The man who invented this indicator, himself, doubts this.

Read more.

Yield curve - Then

Yield curve - Now

Checkout a video on how the yield curve has shot up over this time

Video.

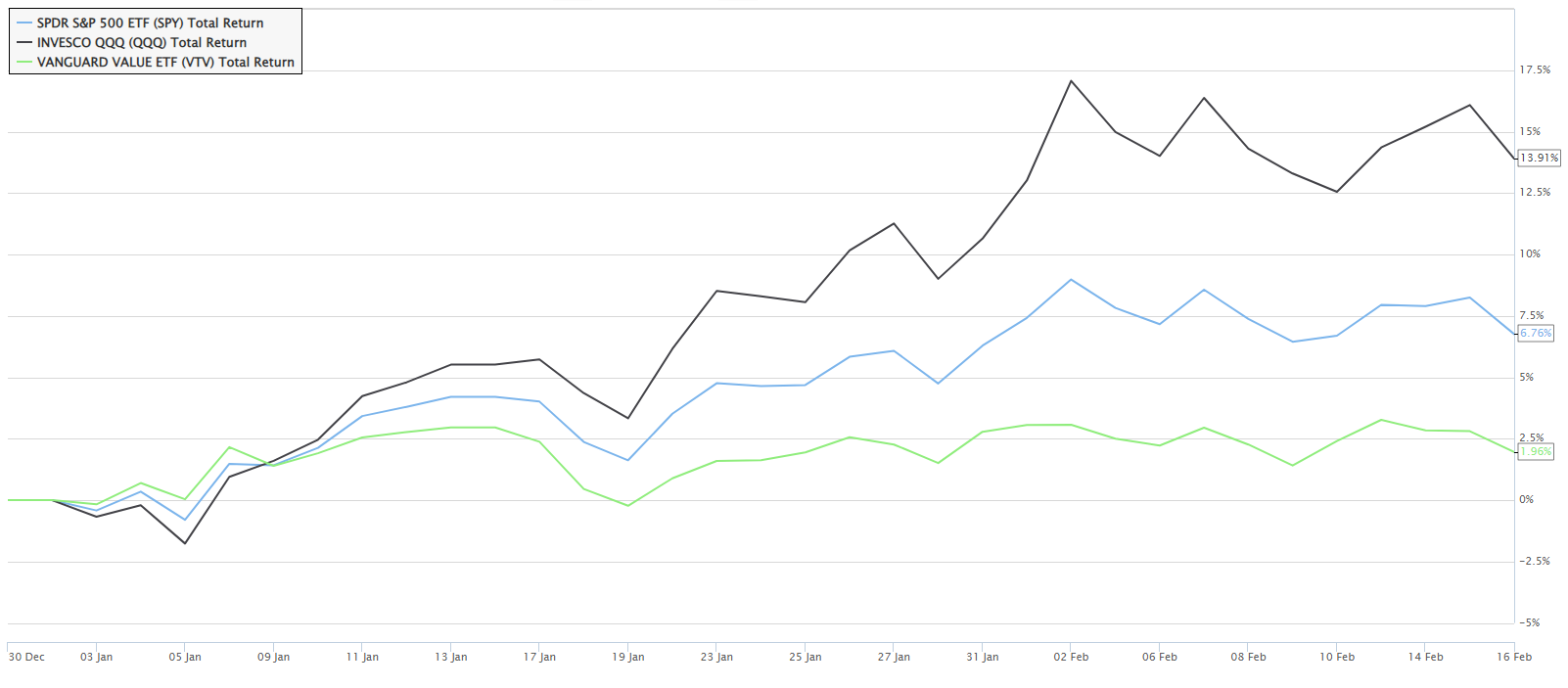

The markets have done well year to date. The earnings season has not been as dismal as expected. The companies

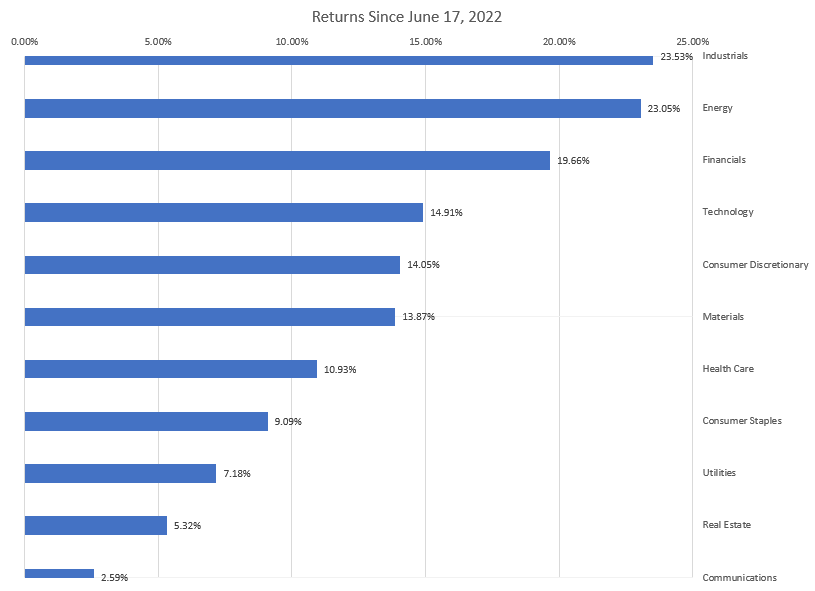

seem to have kick the recession can down the road. The sectors that did badly last year have been outperforming this year.

Energy sector has been the top performer while the Communications sector has been the worst for most of 2022.

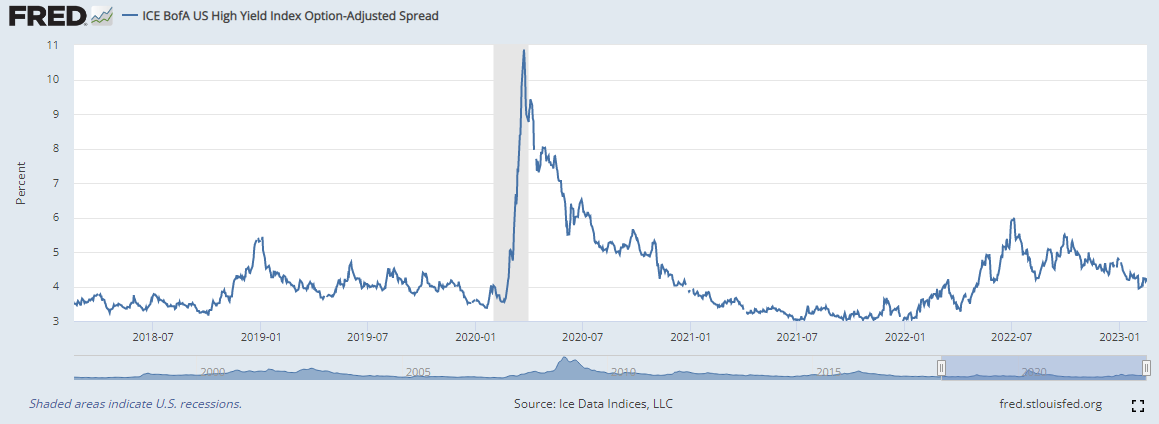

If the economy were to enter a recession, it is likely that some of the companies will struggle to keep up with

their debt payments causing their credit spread to widen. This indicator shows how the credit spreads have been

behaving so far. The credit spreads have been pretty muted so far suggesting a healthy credit market.

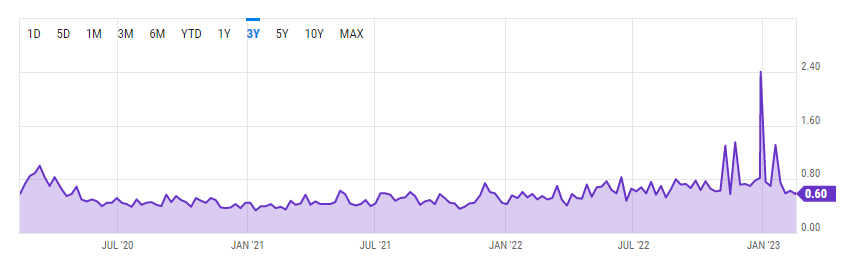

A spike in put / call ratio indicates that investors are very apprehensive about a sudden fall in the equity

markets. In February, the activity has quietened down relative to January.

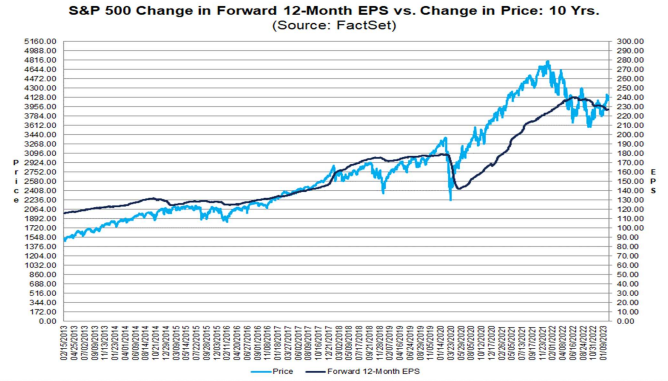

The current earnings forecast by equity analysts estimate the earnings potential for S&P 500 companies to be

around $230 which translates to a price to earnings ratio of 18 at the current S&P 500 price level. This

is above the 10 year average.

It is likely that as inflation comes down, so will the earnings numbers. This indicates that the future S&P 500

price level could likely come down. Based on the companies that have reported so far (82% of S&P 500 companies),

the earnings have declined by -4.7%.

- Trillium Square Advisors LLC is a registered investment adviser offering advisory services in the state of North

Carolina and in other jurisdictions where exempted. Registration as an investment adviser does not imply a

certain level of skill or training, and the content of this communication has not been approved or verified by the

United States Security and Exchange Commission or by any state securities authority.

- Information presented is for educational purposes only and does not intend to make an offer or solicitation for

the sale or purchase of any specific securities, investments or investment strategies. Market data, articles and

other content in this presentation are based on generally available information and are believed to be reliable.

Trillium Square does not guarantee the accuracy of the information contained in this presentation. The

information is of a general nature and should not be construed as investment advice and relied upon in making

investment decisions.

- Investments involve risk and are never guaranteed. Be sure to first consult with a qualified financial adviser before

implementing any strategies discussed herein.

- Past performance is not indicative of future performance.

- The content of this communication and any accompanying documents are confidential. They are not to be copied,

excerpted or distributed without express written permission of the firm. Any other use beyond its author’s intent,

distribution or copying of the contents of this presentation is strictly prohibited. Nothing in this document is

intended to be legal, accounting, or tax advise, and is for informational purposes only.

- Hypothetical performance results have many inherent limitations. No representation is being made that any

account will or is likely to achieve profits or losses similar to those shown. In fact, there are frequently sharp

differences between hypothetical performance results and the actual results subsequently achieved by any

particular investment strategy. Hypothetical performance for illustration purposes only.

- Trillium Square will provide all prospective clients with a copy of our current Form ADV, Part 2A (Disclosure

Brochure) upon request. At anytime you can view our current Form ADV, Part 2A at https://adviserinfo.sec.gov

© Copyright Trillium Square Advisors LLC. All rights reserved.

Main Address:

Trillium Square Advisors LLC,

423 Peaslake Ct, Rolesville NC - 27571

Office Address:

Trillium Square Advisors LLC,

2840 Plaza Place, Suite 210, Raleigh, NC - 27612

Website Content

All written content on this site is for information purposes only. Opinions expressed herein are solely those of Trillium Square Advisors LLC unless otherwise specifically cited. Material presented is believed to be from reliable sources and no representations are made by our firm as to another parties’ informational accuracy or completeness. All information or ideas provided should be discussed in detail with an advisor, accountant or legal counsel prior to implementation.

This website may provide links to others for the convenience of our users. Our firm has no control over the accuracy or content of these other websites.

Registration Information

Advisory services are offered through Trillium Square Advisors LLC; an investment advisor firm domiciled in the State of North Carolina. The presence of this website on the Internet shall not be directly or indirectly interpreted as a solicitation of investment advisory services to persons of another jurisdiction unless otherwise permitted by statute.

Follow-up or individualized responses to consumers in a particular state by our firm in the rendering of personalized investment advice for compensation shall not be made without our first complying with jurisdiction requirements or pursuant to an applicable state exemption.

For information concerning the status or disciplinary history of a broker-dealer, investment advisor, or their representatives, a consumer should contact their state securities administrator.